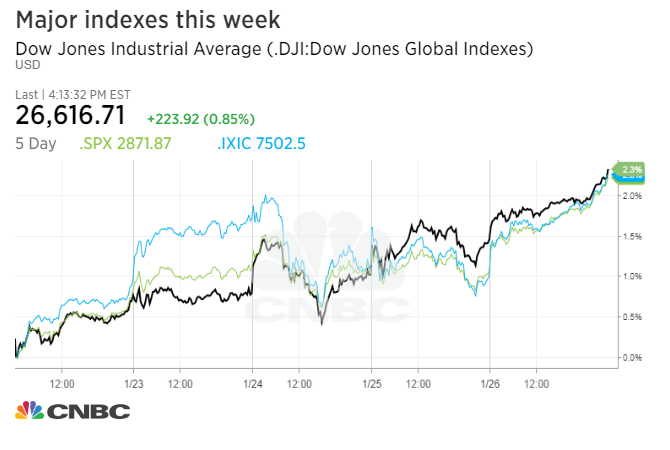

It was another week higher for stocks, but another week with more volatility. Through Friday’s close, the Dow rose 2.1%, the S&P gained 2.2%, and Nasdaq was higher by 2.3%. Falling bond prices (and rising yields) have been a big story for weeks, but the trend stalled this week. Gold saw a positive week, up 1.2%. Oil prices again hit their highest level in three years, up 4.5% this week to close at $66.24 per barrel. The international Brent oil moved own to $70.29.

Markets turned in another week of record gains, but it looked like some jitters crept into trading. There were several days where stocks had solid gains early in the day, only for them to turn and move lower into the close.

Of course, “volatile” is a relative term these days. Stocks are still quiet on a historical basis. The image below shows that it’s been nearly 100 days without a decline of more than 0.6% in the S&P 500. The chart shows just how rare this is.

Of course, “volatile” is a relative term these days. Stocks are still quiet on a historical basis. The image below shows that it’s been nearly 100 days without a decline of more than 0.6% in the S&P 500. The chart shows just how rare this is.

Even more incredibly, it’s been almost 200 days since we’ve had back-to-back losses of more than 0.25% in the S&P. The chart below again shows how rare these conditions are.

Getting into the events of the week, much of the attention was on business and political leaders gathered in Davos for the World Economic Forum. Attendees gather here annually to discuss the pressing issues of the world – though we often question if anything tangible ever comes from these events.

A big topic of discussion has been the strength of the U.S. dollar. Heading into this week, the dollar was already at three-year lows.

A big topic of discussion has been the strength of the U.S. dollar. Heading into this week, the dollar was already at three-year lows.

This is unusual since currencies tend to reflect the strength of an economy and with ours improving, normally the dollar would be strengthening.

Why does this matter? First, it makes commodities and imports more expensive because it takes more dollars to buy that product. This is part of the reason why oil prices have risen. The weak dollar also reduces the amount of investment in the U.S. by foreign investors and makes our borrowing costs rise (through higher interest rates).

However, large U.S. businesses like a weaker currency because it makes their products more attractive to shoppers overseas since they will cost less.

At any rate, the topic of the dollar dominated headlines after Treasury Secretary Steve Mnuchen was quoted as saying the weaker dollar was good for the U.S. and helps our exports. This was newsworthy because historically Treasury Secretary’s only say the U.S. supports a stronger dollar. The dollar dropped even further after the reports.

Why does this matter? First, it makes commodities and imports more expensive because it takes more dollars to buy that product. This is part of the reason why oil prices have risen. The weak dollar also reduces the amount of investment in the U.S. by foreign investors and makes our borrowing costs rise (through higher interest rates).

However, large U.S. businesses like a weaker currency because it makes their products more attractive to shoppers overseas since they will cost less.

At any rate, the topic of the dollar dominated headlines after Treasury Secretary Steve Mnuchen was quoted as saying the weaker dollar was good for the U.S. and helps our exports. This was newsworthy because historically Treasury Secretary’s only say the U.S. supports a stronger dollar. The dollar dropped even further after the reports.

After the news broke, Secretary Mnuchen quickly noted that these comments were taken out of context. He said the U.S. does support a strong dollar – in the long run – but that we have little impact on the currency in the short run – which is true, though is not often mentioned.

President Trump was also quick to clarify and the remarks halted the dollar’s decline.

Back here at home, investors had their eyes on several economic reports. Data on housing showed the pace of homes sales declined last month, but capped off the best year since 2006 for existing home sales and 2007 for new home sales. Also, data on durable goods showed an increase from the previous month.

The big report came on Friday with the release of fourth quarter GDP data. Economists were expecting a number around 3%, only to be disappointed with a print of 2.6%. Digging into the individual components, however, showed there was a lot of strength. The big detractor to the GDP number was imports. Last quarter had the largest amount of imports since 2010, which took almost two points off that 2.6% number.

The big report came on Friday with the release of fourth quarter GDP data. Economists were expecting a number around 3%, only to be disappointed with a print of 2.6%. Digging into the individual components, however, showed there was a lot of strength. The big detractor to the GDP number was imports. Last quarter had the largest amount of imports since 2010, which took almost two points off that 2.6% number.

Next Week

Next week will be a busy one. On the economic side, we’ll get info on housing, personal income and spending, the strength of the manufacturing sector, and the always-important employment report. The Fed will also be holding a policy meeting. No changes to their policy are expected, but investors will be watching for clues on future policy changes.

We’re also in the busy part of earnings season, so there will be a lot of company-specific news for investors to digest.

Finally, the State of the Union address from President Trump is likely to have people talking. His performance this week in Davos was solid and helped the markets and will likely do the same with a solid performance again this week.

Investment Strategy

We continue to believe markets are at very high levels here. Last week some of the indicators we follow showed stalling, but they improved again this week. There doesn’t seem to be a lot of red flags out there for the market (which in itself could be seen as a red flag). We don’t see a large drop on the horizon, but are cautious about putting new money into the broader market at this point.

We are positive on the market and economy in the longer term, too, as pro-business policies will be beneficial to businesses.

Bond prices have trended lower (and yields higher) the last few months and are now around their lowest level in three years. We’ll be looking to see if buyers step in here to buy at these low prices and higher yields as they have done in the past, or if this is a shift in the bond market and prices will keep falling.

As for the rest of the portfolio, bonds to protect against inflation, or TIPs, remain a good long term hedge for inflation. Floating-rate bonds will do well if interest rates eventually do rise.

Some municipal bonds look attractive for the right client, too. We like buying individual, insured names for these bonds, avoiding muni index bonds if possible. We keep a longer term focus with these investments.

Gold is another good hedge for the portfolio. It is only a hedge at this point – rising on geopolitical issues as a flight to safety.

Finally, in international stocks, we prefer developed markets to emerging ones at this time.

This commentary is for informational purposes and is not investment advice, an indicator of future performance, a solicitation, an offer to buy or sell, or a recommendation for any security. It should not be used as a primary basis for making investment decisions. Consider your own financial circumstances and goals carefully before investing. Past performance cannot guarantee results.

Next week will be a busy one. On the economic side, we’ll get info on housing, personal income and spending, the strength of the manufacturing sector, and the always-important employment report. The Fed will also be holding a policy meeting. No changes to their policy are expected, but investors will be watching for clues on future policy changes.

We’re also in the busy part of earnings season, so there will be a lot of company-specific news for investors to digest.

Finally, the State of the Union address from President Trump is likely to have people talking. His performance this week in Davos was solid and helped the markets and will likely do the same with a solid performance again this week.

Investment Strategy

We continue to believe markets are at very high levels here. Last week some of the indicators we follow showed stalling, but they improved again this week. There doesn’t seem to be a lot of red flags out there for the market (which in itself could be seen as a red flag). We don’t see a large drop on the horizon, but are cautious about putting new money into the broader market at this point.

We are positive on the market and economy in the longer term, too, as pro-business policies will be beneficial to businesses.

Bond prices have trended lower (and yields higher) the last few months and are now around their lowest level in three years. We’ll be looking to see if buyers step in here to buy at these low prices and higher yields as they have done in the past, or if this is a shift in the bond market and prices will keep falling.

As for the rest of the portfolio, bonds to protect against inflation, or TIPs, remain a good long term hedge for inflation. Floating-rate bonds will do well if interest rates eventually do rise.

Some municipal bonds look attractive for the right client, too. We like buying individual, insured names for these bonds, avoiding muni index bonds if possible. We keep a longer term focus with these investments.

Gold is another good hedge for the portfolio. It is only a hedge at this point – rising on geopolitical issues as a flight to safety.

Finally, in international stocks, we prefer developed markets to emerging ones at this time.

This commentary is for informational purposes and is not investment advice, an indicator of future performance, a solicitation, an offer to buy or sell, or a recommendation for any security. It should not be used as a primary basis for making investment decisions. Consider your own financial circumstances and goals carefully before investing. Past performance cannot guarantee results.