A late-day decline Friday put stocks in the red for the week. Through the close, the Dow was lower by 0.3%, the S&P was off a slight 0.1%, while the Nasdaq turned in a more respectable 0.5% gain. Gold keeps climbing higher, up 0.4% this week. We are seeing higher gas prices at the pump as oil continues to climb, up 2.1% this week to $102.20 per barrel. The international Brent oil, used for much of our gas here in the east, rose to $109.84.

Source: Yahoo Finance (the chart is skewed this week due to the Monday holiday)

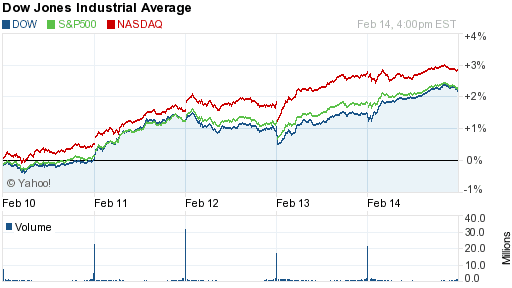

The gains we’ve seen in the market over the last few weeks shows us there is a lot less worry than at the beginning of the year. Though the gains stalled this week, stocks still shrugged off bad news and held their ground.

The actions of the Fed still seem to be an important driver of the market. The minutes from the latest Fed meeting were released this week, indicating the reduction in stimulus would continue. The info was nothing new. However, stocks dropped sharply on the news Wednesday, as can be seen in the chart above.

It looks like many investors are hoping the Fed will stop its reduction of stimulus, even hoping for more in light of the poor economic reports. The Fed seems resolute in pulling back, as the minutes made clear. They even discussed raising interest rates, which is highly unlikely any time soon, but just the mention was enough to worry the market.

There were several economic reports released this week, and none were good. Of course the weather has been cited as a factor, although its impact is questionable. Manufacturing in the New York and Philadelphia regions dropped sharply, and a legitimate argument can be made that weather had an impact on these figures.

However, housing data continues to deteriorate nationwide, including areas not affected by the poor weather. In fact, the areas not affected by the weather showed the worst decline, indicating that weather is not a factor.

Also, inflation figures released this week showed a slight gain, but the comparisons have become cloudy due to a new methodology in computing inflation. The new method includes more items and claims to be more robust, but we know there are never changes in methodology unless it skews to the governments favor. As any regular shopper can attest, inflation is many times higher than advertised.

Finally, a stock story that makes us worry the market is becoming irrationally overvalued. This week Facebook announced it was purchasing a text message service called WhatsApp. The service claims to have 450 million users, and showing how knowledgeable we are about social media, we had never heard of it.

What raised eyebrows is the price Facebook paid. This text message service, with 50 employees, was purchased for $19 billion ($16B in cash and stock, $3B in restricted stock). Facebook is paying more than two times its annual revenue for a company with barely any revenue.

Just for comparison, the valuation of this text message service is higher than many other companies you are familiar with. It’s worth more than ConAgra, for instance, which has 26,000 employees. Or airlines like Southwest and American. Or clothing companies like the Gap, Ralph Lauren, and Under Armour. Or Lowes home improvement stores. Or Campbell’s Soup. Harley Davidson. Xerox. We could go on, but you get the point.

This extremely high valuation is reminiscent of the tech bubble in the late 1990’s and makes us worry.

Next Week

We’ll see a handful of economic reports next week, including data on housing, durable goods, and consumer confidence. Getting more attention will be the new Fed chief Janet Yellen’s testimony in front of the Senate. We don’t think we’ll learn anything new, but as we saw with the minutes released this week, investors are hoping for an end to the reduction in stimulus.

Investment Strategy

Despite going nowhere this week, in the short run, we think the market has a better chance to move to the upside than downside. In the longer run, we worry that the economy is not as great as many think and other issues like a slowdown in China will cause additional problems. However, we’ve held this view for some time and the market has continued to move higher.

Being value investors by nature, we like buying on dips and wouldn’t put new money into the broader market at this point. We still see many undervalued individual names to invest in, however. We mentioned our concerns for the longer run, so we are keeping an eye out for trouble and will look to exit if it surfaces.

As for bonds, yields continue to hover around these current levels and trying to figure out where they’ll go from here is a guessing game, at best. Bonds will always have their place in a portfolio, but there is a worry about rates rising (so prices would fall). A short position (bet on the decline in prices) acts as a nice hedge if yields do rise. Floating rate bonds are also gaining popularity for this same reason, but they tend to be riskier investments, so caution is warranted.

Continuing with bonds, TIPs remain an important hedge against future inflation and municipal bonds are in the same boat and work for the right client. We like buying individual, insured names for these bonds, avoiding muni index bonds if possible. We keep a longer term focus with these investments.

Gold again reached its highest level in three months and has performed well recently. It remains volatile, so we’d still be cautious, but it acts as a good hedge in the longer run.

We like other commodities for the long term, especially due to weaker currencies around the globe. This is a longer-term play, so buying on the dips may work with a longer time horizon.

Finally, in international stocks, we see weakness around the globe and favor neither the developed or emerging markets.

Please note, these day-to-day and week-to-week fluctuations have little impact on positions we intend to hold for several years or longer. Our short and medium term investments are the only positions affected by these daily and weekly fluctuations.

This commentary is for informational purposes and is not investment advice, an indicator of future performance, a solicitation, an offer to buy or sell, or a recommendation for any security. It should not be used as a primary basis for making investment decisions. Consider your own financial circumstances and goals carefully before investing. Past performance cannot guarantee results.

The actions of the Fed still seem to be an important driver of the market. The minutes from the latest Fed meeting were released this week, indicating the reduction in stimulus would continue. The info was nothing new. However, stocks dropped sharply on the news Wednesday, as can be seen in the chart above.

It looks like many investors are hoping the Fed will stop its reduction of stimulus, even hoping for more in light of the poor economic reports. The Fed seems resolute in pulling back, as the minutes made clear. They even discussed raising interest rates, which is highly unlikely any time soon, but just the mention was enough to worry the market.

There were several economic reports released this week, and none were good. Of course the weather has been cited as a factor, although its impact is questionable. Manufacturing in the New York and Philadelphia regions dropped sharply, and a legitimate argument can be made that weather had an impact on these figures.

However, housing data continues to deteriorate nationwide, including areas not affected by the poor weather. In fact, the areas not affected by the weather showed the worst decline, indicating that weather is not a factor.

Also, inflation figures released this week showed a slight gain, but the comparisons have become cloudy due to a new methodology in computing inflation. The new method includes more items and claims to be more robust, but we know there are never changes in methodology unless it skews to the governments favor. As any regular shopper can attest, inflation is many times higher than advertised.

Finally, a stock story that makes us worry the market is becoming irrationally overvalued. This week Facebook announced it was purchasing a text message service called WhatsApp. The service claims to have 450 million users, and showing how knowledgeable we are about social media, we had never heard of it.

What raised eyebrows is the price Facebook paid. This text message service, with 50 employees, was purchased for $19 billion ($16B in cash and stock, $3B in restricted stock). Facebook is paying more than two times its annual revenue for a company with barely any revenue.

Just for comparison, the valuation of this text message service is higher than many other companies you are familiar with. It’s worth more than ConAgra, for instance, which has 26,000 employees. Or airlines like Southwest and American. Or clothing companies like the Gap, Ralph Lauren, and Under Armour. Or Lowes home improvement stores. Or Campbell’s Soup. Harley Davidson. Xerox. We could go on, but you get the point.

This extremely high valuation is reminiscent of the tech bubble in the late 1990’s and makes us worry.

Next Week

We’ll see a handful of economic reports next week, including data on housing, durable goods, and consumer confidence. Getting more attention will be the new Fed chief Janet Yellen’s testimony in front of the Senate. We don’t think we’ll learn anything new, but as we saw with the minutes released this week, investors are hoping for an end to the reduction in stimulus.

Investment Strategy

Despite going nowhere this week, in the short run, we think the market has a better chance to move to the upside than downside. In the longer run, we worry that the economy is not as great as many think and other issues like a slowdown in China will cause additional problems. However, we’ve held this view for some time and the market has continued to move higher.

Being value investors by nature, we like buying on dips and wouldn’t put new money into the broader market at this point. We still see many undervalued individual names to invest in, however. We mentioned our concerns for the longer run, so we are keeping an eye out for trouble and will look to exit if it surfaces.

As for bonds, yields continue to hover around these current levels and trying to figure out where they’ll go from here is a guessing game, at best. Bonds will always have their place in a portfolio, but there is a worry about rates rising (so prices would fall). A short position (bet on the decline in prices) acts as a nice hedge if yields do rise. Floating rate bonds are also gaining popularity for this same reason, but they tend to be riskier investments, so caution is warranted.

Continuing with bonds, TIPs remain an important hedge against future inflation and municipal bonds are in the same boat and work for the right client. We like buying individual, insured names for these bonds, avoiding muni index bonds if possible. We keep a longer term focus with these investments.

Gold again reached its highest level in three months and has performed well recently. It remains volatile, so we’d still be cautious, but it acts as a good hedge in the longer run.

We like other commodities for the long term, especially due to weaker currencies around the globe. This is a longer-term play, so buying on the dips may work with a longer time horizon.

Finally, in international stocks, we see weakness around the globe and favor neither the developed or emerging markets.

Please note, these day-to-day and week-to-week fluctuations have little impact on positions we intend to hold for several years or longer. Our short and medium term investments are the only positions affected by these daily and weekly fluctuations.

This commentary is for informational purposes and is not investment advice, an indicator of future performance, a solicitation, an offer to buy or sell, or a recommendation for any security. It should not be used as a primary basis for making investment decisions. Consider your own financial circumstances and goals carefully before investing. Past performance cannot guarantee results.