It was a strong week for the stock market with new multi-year highs reached. For the week, the Dow gained 1.7%, the S&P rose 2.2%, and the Nasdaq returned 2.3%. The promise of further money printing resulted in another week of solid gains for gold, rising 3.1% to a six-month high. Oil saw little change, losing just 0.05% to close above $96 per barrel. The other major type of oil, Brent, closed at $114.60 per barrel.

Source: MSN Moneycentral

Though the week got off to a rough start, news out of Europe sent the markets to multi-year highs. The Dow and S&P reached levels not seen in more than five years, while the Nasdaq reached an even more impressive 12-year high.

The week opened with reports showing an increasing weakness in global growth. Manufacturing growth in Asia is slowing, while Europe and the US show contraction. In fact, a report showed that 80% of the world’s economies are contracting.

FedEx supported that view. With their shipping seen as a barometer for growth, they warned of a slowdown, particularly in China.

Coming off that sour news, investors were pinning their hopes on more stimulus from the European Central Bank (or ECB). As you can see in the chart above, Thursday’s gains show they were not disappointed.

To bring down borrowing costs for troubled European countries, the ECB announced an unlimited purchase of shorter dated bonds (this is similar to what our Fed has done). The action eliminated the risk of a Euro breakup in the near term and the markets shot higher.

Essentially this action is printing money. One caveat is that they will counter the money printing by taking money out of the system by selling longer term bonds. Theoretically, no new money will enter the economy and should eliminate any potential inflation. However, many analysts realize this is largely symbolic since banks can continue to borrow from the ECB, increasing the money supply.

Another problem is that the ECB is prohibited from directly buying bonds of countries, which is considered financing of that government. Yet that is what they are doing. To bypass that condition, they decided any bonds under three years don’t constitute financing. This is a completely arbitrary number designed to circumvent the rules and many are not pleased.

Germany has been vocal in their criticism, largely because they are on the hook for the profligate countries. Actually, it has lead to disagreement within Germany, since some are opposed and others support the action. Next week will give us a better idea which way the country will lean as their courts rule on the constitutionality of the bailout.

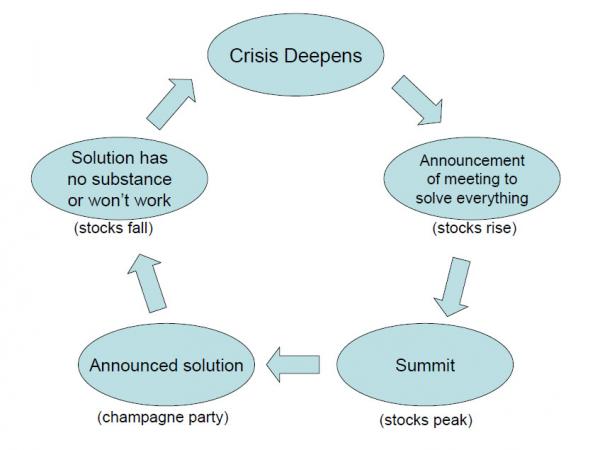

At the end of the day, it’s not likely these steps will be any more successful than past actions. We’ve seen this story several times before. Some sort of bailout is announced, the market rallies. Then no surprise, throwing more money at the problem fails to achieve any lasting improvements. The market sinks and the cycle begins again. Hedge fund manager David Einhorn created a great graphic that illustrates this cycle, seen below.

The week opened with reports showing an increasing weakness in global growth. Manufacturing growth in Asia is slowing, while Europe and the US show contraction. In fact, a report showed that 80% of the world’s economies are contracting.

FedEx supported that view. With their shipping seen as a barometer for growth, they warned of a slowdown, particularly in China.

Coming off that sour news, investors were pinning their hopes on more stimulus from the European Central Bank (or ECB). As you can see in the chart above, Thursday’s gains show they were not disappointed.

To bring down borrowing costs for troubled European countries, the ECB announced an unlimited purchase of shorter dated bonds (this is similar to what our Fed has done). The action eliminated the risk of a Euro breakup in the near term and the markets shot higher.

Essentially this action is printing money. One caveat is that they will counter the money printing by taking money out of the system by selling longer term bonds. Theoretically, no new money will enter the economy and should eliminate any potential inflation. However, many analysts realize this is largely symbolic since banks can continue to borrow from the ECB, increasing the money supply.

Another problem is that the ECB is prohibited from directly buying bonds of countries, which is considered financing of that government. Yet that is what they are doing. To bypass that condition, they decided any bonds under three years don’t constitute financing. This is a completely arbitrary number designed to circumvent the rules and many are not pleased.

Germany has been vocal in their criticism, largely because they are on the hook for the profligate countries. Actually, it has lead to disagreement within Germany, since some are opposed and others support the action. Next week will give us a better idea which way the country will lean as their courts rule on the constitutionality of the bailout.

At the end of the day, it’s not likely these steps will be any more successful than past actions. We’ve seen this story several times before. Some sort of bailout is announced, the market rallies. Then no surprise, throwing more money at the problem fails to achieve any lasting improvements. The market sinks and the cycle begins again. Hedge fund manager David Einhorn created a great graphic that illustrates this cycle, seen below.

We closed out the week with a disappointing report on jobs in the US. For the month of August, the economy added a paltry 96,000 jobs. This was far lower than estimates and even further below the level needed just to keep up with the growth in population.

Though the unemployment rate fell to 8.1% from 8.3%, the drop can be attributed to a plunge in labor participation. Our labor force now stands at a 31-year low. If we were to measure the unemployment rate using the labor force size from the beginning of the recession, that number would be closer to 12%, not 8.1%.

Next Week

These negative economic reports have increased the likelihood of stimulus from the Fed here in the US. Next week will be very important for this subject as the Fed holds another scheduled meeting where this topic will be front and center.

Many to most market participants predict an announcement from Fed Chief Bernanke on a new round of stimulus. If such an announcement is made, we should see a significant gain in the market. If not, the reverse is true. Either way, next week could see some relatively large moves.

As for economic data next week, there will be several reports worth noting. We will get info on consumer credit, small business optimism, industrial production, and inflation with the CPI and PPI.

Investment Strategy

As this week has shown, the market is highly reliant on central banks for direction. For this reason, it is difficult to have strong convictions either way due to the unpredictable nature of their actions. Next week will be important for this very reason. If stimulus is announced, the market will rally. If not, it will head lower. Odds are high that a new stimulus will be announced, so there is potentially a bigger risk to the downside.

One thing can be said for sure, any stimulus actions will have a limited effect. We’ve seen it many times now, both here and abroad. The market will rally for a short time but ultimately fall when it wears off. Stimulus does nothing to fundamentally help the economy and possibly does more damage than good.

But it does send the market higher in the short term and we don’t want to be on the wrong side of that trade. Like before, agility remains important.

If we were to get a buying opportunity, we still like large cap higher-quality and dividend paying stocks. Smaller and little-known stocks with low correlation to the market (and Europe) are also promising. There is always the opportunity to find an undervalued individual stock at any time, as well.

We like gold for the long term, as it will do well with debt problems, further bailouts, and stimulus programs. The recent rally has decreased our chances of adding to our position (and we aren’t looking to sell), but we would add if prices moved much lower from here.

We like other commodities for the long term but fear a slowdown in China and the other BRIC countries (Brazil, Russia, and India), will result in lower prices in the short term.

With Treasury bonds near historic lows (so prices are near historic highs), a short position (bet on a decline in price) only provides a nice hedge here and we believe the potential for profit is low at this time.

On the bond theme, we think TIPs are important as we still expect inflation to increase. Municipal bonds also work and there are some nice yielding bonds out there now (try to avoid muni funds and buy the actual bond if possible), though our concern has increased as the pace of distressed municipalities is increasing. Additionally, higher taxes from the health care law will increase the attractiveness of these bonds in the future.

Finally, in international stocks, we favor developed international markets as opposed to emerging.

These day-to-day and week-to-week fluctuations have little impact on positions we intend to hold for several years or longer. Our short and medium term investments are the only positions affected by these daily and weekly fluctuations.

This commentary is for informational purposes and is not investment advice, an indicator of future performance, a solicitation, an offer to buy or sell, or a recommendation for any security. It should not be used as a primary basis for making investment decisions. Consider your own financial circumstances and goals carefully before investing. Past performance cannot guarantee results.

Though the unemployment rate fell to 8.1% from 8.3%, the drop can be attributed to a plunge in labor participation. Our labor force now stands at a 31-year low. If we were to measure the unemployment rate using the labor force size from the beginning of the recession, that number would be closer to 12%, not 8.1%.

Next Week

These negative economic reports have increased the likelihood of stimulus from the Fed here in the US. Next week will be very important for this subject as the Fed holds another scheduled meeting where this topic will be front and center.

Many to most market participants predict an announcement from Fed Chief Bernanke on a new round of stimulus. If such an announcement is made, we should see a significant gain in the market. If not, the reverse is true. Either way, next week could see some relatively large moves.

As for economic data next week, there will be several reports worth noting. We will get info on consumer credit, small business optimism, industrial production, and inflation with the CPI and PPI.

Investment Strategy

As this week has shown, the market is highly reliant on central banks for direction. For this reason, it is difficult to have strong convictions either way due to the unpredictable nature of their actions. Next week will be important for this very reason. If stimulus is announced, the market will rally. If not, it will head lower. Odds are high that a new stimulus will be announced, so there is potentially a bigger risk to the downside.

One thing can be said for sure, any stimulus actions will have a limited effect. We’ve seen it many times now, both here and abroad. The market will rally for a short time but ultimately fall when it wears off. Stimulus does nothing to fundamentally help the economy and possibly does more damage than good.

But it does send the market higher in the short term and we don’t want to be on the wrong side of that trade. Like before, agility remains important.

If we were to get a buying opportunity, we still like large cap higher-quality and dividend paying stocks. Smaller and little-known stocks with low correlation to the market (and Europe) are also promising. There is always the opportunity to find an undervalued individual stock at any time, as well.

We like gold for the long term, as it will do well with debt problems, further bailouts, and stimulus programs. The recent rally has decreased our chances of adding to our position (and we aren’t looking to sell), but we would add if prices moved much lower from here.

We like other commodities for the long term but fear a slowdown in China and the other BRIC countries (Brazil, Russia, and India), will result in lower prices in the short term.

With Treasury bonds near historic lows (so prices are near historic highs), a short position (bet on a decline in price) only provides a nice hedge here and we believe the potential for profit is low at this time.

On the bond theme, we think TIPs are important as we still expect inflation to increase. Municipal bonds also work and there are some nice yielding bonds out there now (try to avoid muni funds and buy the actual bond if possible), though our concern has increased as the pace of distressed municipalities is increasing. Additionally, higher taxes from the health care law will increase the attractiveness of these bonds in the future.

Finally, in international stocks, we favor developed international markets as opposed to emerging.

These day-to-day and week-to-week fluctuations have little impact on positions we intend to hold for several years or longer. Our short and medium term investments are the only positions affected by these daily and weekly fluctuations.

This commentary is for informational purposes and is not investment advice, an indicator of future performance, a solicitation, an offer to buy or sell, or a recommendation for any security. It should not be used as a primary basis for making investment decisions. Consider your own financial circumstances and goals carefully before investing. Past performance cannot guarantee results.