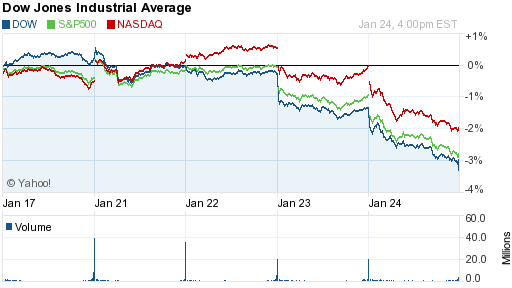

The sell-off in stocks accelerated this week, turning in their worst performance since 2011. Through the close Friday, the Dow plunged 3.5%, the S&P dropped 2.6%, and the Nasdaq was lower by 1.7%. For bonds, government bonds rose and yields fell to the lowest level in two months. Gold was the big winner of the week, rising 1.0% to hit a two-month high. Oil prices also rose, gaining 2.2% to $96.64 per barrel. The international Brent crude, used in much of our gas here in the East, move higher to just under $108 per barrel.

Source: Yahoo Finance

When central banks around the globe flooded the markets with money, it flowed to places it normally wouldn’t go and papered over serious underlying problems. The end of every stimulus program has played out the same way - the problems resurface and markets collapse. It looks like it is playing out again.

The issues this week started in China. Recent economic reports have showed a weakening economy and a new report this week revealed a contraction in their manufacturing sector. Since China is notorious for fudging their numbers, admitting to a decline makes us sure it is worse than it appears.

This, combined with the lower liquidity from our central bank, fueled concerns of defaults within the country. It is something to pay attention to, since China has massive amounts of loans through their shadow banking system.

Other emerging market countries were hit especially hard this week. They have benefitted greatly from the stimulus programs, as new funds flowed into these countries looking for returns. As the stimulus is reduced, these countries are the first and hardest to get hit. We saw this play out with India the last time there was talk of reducing stimulus.

This time it was countries with large current account deficits, or countries that import more than they export. Currencies in countries like Argentina, Turkey, Russia, South Africa, and Mexico plunged severely this week. It is a very serious issue for these economies.

Why should we be concerned about currencies of these relatively unimportant countries? Back in 1997, the currency of Thailand, the Baht, plunged and triggered a currency crisis and global sell-off. It also happened in 1994 with the Mexican Peso. These countries may be small players on a global scale, but currency problems can ripple through the global economy.

This is a downside of these stimulus programs – fundamental changes are needed to address the cause these crises, but the flood of money does not force governments to do so.

It takes a pullback in stimulus to reveal how poor the global economy really is. Unfortunately, that causes markets to fall and central banks step back in to resume the stimulus programs as the cycle continues. Eventually we think this will end very badly.

This makes next week very important. The Fed is holding another policy meeting and economists have widely expected another pullback in their stimulus program. The question is, will the events of this week prevent another pullback? Is it possible they will increase the stimulus? Whatever the answer, the market will be paying close attention to their decision.

As for other news this week, there was very little in terms of economic data, but there were many corporate earnings releases. Remember, the bar was set very high here and the actual results have been pretty lackluster. According to Factset, earnings have grown 6.4%, which sounds good. Investors weren’t excited though, as revenue (or what the company actually earned in sales) grew at just 0.7%. The lack of excitement likely played a part in the market decline this week.

Next Week

Next week will be another busy one. As mentioned above, investors will be closely watching the Fed meeting for their decision on reducing stimulus. Additionally, another quarter of the S&P 500 stocks will be releasing their corporate earnings. Adding to the already busy week, we will get economic reports on housing, durable goods, personal income and spending, and fourth quarter GDP.

One other item to consider as we close out the month is the “January effect.” The old saying is “As goes January, so goes the year.” If January closes with a gain, or vice-versa, history has shown there is a 90% chance of closing the year in the same direction. With the Dow down over 4% and the S&P down over 3%, they’ll need to put in a solid performance this week to have a better shot at closing the year higher. At least, that’s how the saying goes.

Investment Strategy

We’ve been cautious on the market recently, but if stocks come off a little further, they could present a good buying opportunity. We’d like to see some support, meaning some buying to come in, before we would put any new money here. This would be a short-term play, too. We have serious concerns for the long run, especially when these stimulus programs run their course.

In the meantime, we still prefer finding undervalued individual names to invest in. Fundamental analysis tells us how good a company is, while the technical (or the charts) side gives us a good idea of when to buy. We would avoid stocks in sectors with a strong correlation to the broader stock market and interest rates. Our timeframe is shorter (looking out a couple weeks or months), so we can keep one foot out the door in case the market turns abruptly.

Bonds yields moved lower this week (so prices rose). A short position (bet on the decline in prices) didn’t fare too well here, but still acts as a nice hedge. It isn’t intended to be a longer term investment.

Continuing with bonds, TIPs have shown weakness recently, however, they remain an important hedge against future inflation. Municipal bonds are in the same boat and work for the right client. We like buying individual, insured names for these bonds, avoiding muni index bonds if possible. We keep a longer term focus with these investments.

Gold turned in another nice week, but has been stuck in the $1,200-1,300 range for many weeks now. It’s good as a long term hedge, and performed nicely as the market fell, but there may still be weakness in the short term.

We like other commodities for the long term, especially due to weaker currencies around the globe. This is a longer-term play, so buying on the dips may work with a longer time horizon.

Finally, in international stocks, we see weakness around the globe and favor neither the developed or emerging markets.

Please note, these day-to-day and week-to-week fluctuations have little impact on positions we intend to hold for several years or longer. Our short and medium term investments are the only positions affected by these daily and weekly fluctuations.

This commentary is for informational purposes and is not investment advice, an indicator of future performance, a solicitation, an offer to buy or sell, or a recommendation for any security. It should not be used as a primary basis for making investment decisions. Consider your own financial circumstances and goals carefully before investing. Past performance cannot guarantee results.

The issues this week started in China. Recent economic reports have showed a weakening economy and a new report this week revealed a contraction in their manufacturing sector. Since China is notorious for fudging their numbers, admitting to a decline makes us sure it is worse than it appears.

This, combined with the lower liquidity from our central bank, fueled concerns of defaults within the country. It is something to pay attention to, since China has massive amounts of loans through their shadow banking system.

Other emerging market countries were hit especially hard this week. They have benefitted greatly from the stimulus programs, as new funds flowed into these countries looking for returns. As the stimulus is reduced, these countries are the first and hardest to get hit. We saw this play out with India the last time there was talk of reducing stimulus.

This time it was countries with large current account deficits, or countries that import more than they export. Currencies in countries like Argentina, Turkey, Russia, South Africa, and Mexico plunged severely this week. It is a very serious issue for these economies.

Why should we be concerned about currencies of these relatively unimportant countries? Back in 1997, the currency of Thailand, the Baht, plunged and triggered a currency crisis and global sell-off. It also happened in 1994 with the Mexican Peso. These countries may be small players on a global scale, but currency problems can ripple through the global economy.

This is a downside of these stimulus programs – fundamental changes are needed to address the cause these crises, but the flood of money does not force governments to do so.

It takes a pullback in stimulus to reveal how poor the global economy really is. Unfortunately, that causes markets to fall and central banks step back in to resume the stimulus programs as the cycle continues. Eventually we think this will end very badly.

This makes next week very important. The Fed is holding another policy meeting and economists have widely expected another pullback in their stimulus program. The question is, will the events of this week prevent another pullback? Is it possible they will increase the stimulus? Whatever the answer, the market will be paying close attention to their decision.

As for other news this week, there was very little in terms of economic data, but there were many corporate earnings releases. Remember, the bar was set very high here and the actual results have been pretty lackluster. According to Factset, earnings have grown 6.4%, which sounds good. Investors weren’t excited though, as revenue (or what the company actually earned in sales) grew at just 0.7%. The lack of excitement likely played a part in the market decline this week.

Next Week

Next week will be another busy one. As mentioned above, investors will be closely watching the Fed meeting for their decision on reducing stimulus. Additionally, another quarter of the S&P 500 stocks will be releasing their corporate earnings. Adding to the already busy week, we will get economic reports on housing, durable goods, personal income and spending, and fourth quarter GDP.

One other item to consider as we close out the month is the “January effect.” The old saying is “As goes January, so goes the year.” If January closes with a gain, or vice-versa, history has shown there is a 90% chance of closing the year in the same direction. With the Dow down over 4% and the S&P down over 3%, they’ll need to put in a solid performance this week to have a better shot at closing the year higher. At least, that’s how the saying goes.

Investment Strategy

We’ve been cautious on the market recently, but if stocks come off a little further, they could present a good buying opportunity. We’d like to see some support, meaning some buying to come in, before we would put any new money here. This would be a short-term play, too. We have serious concerns for the long run, especially when these stimulus programs run their course.

In the meantime, we still prefer finding undervalued individual names to invest in. Fundamental analysis tells us how good a company is, while the technical (or the charts) side gives us a good idea of when to buy. We would avoid stocks in sectors with a strong correlation to the broader stock market and interest rates. Our timeframe is shorter (looking out a couple weeks or months), so we can keep one foot out the door in case the market turns abruptly.

Bonds yields moved lower this week (so prices rose). A short position (bet on the decline in prices) didn’t fare too well here, but still acts as a nice hedge. It isn’t intended to be a longer term investment.

Continuing with bonds, TIPs have shown weakness recently, however, they remain an important hedge against future inflation. Municipal bonds are in the same boat and work for the right client. We like buying individual, insured names for these bonds, avoiding muni index bonds if possible. We keep a longer term focus with these investments.

Gold turned in another nice week, but has been stuck in the $1,200-1,300 range for many weeks now. It’s good as a long term hedge, and performed nicely as the market fell, but there may still be weakness in the short term.

We like other commodities for the long term, especially due to weaker currencies around the globe. This is a longer-term play, so buying on the dips may work with a longer time horizon.

Finally, in international stocks, we see weakness around the globe and favor neither the developed or emerging markets.

Please note, these day-to-day and week-to-week fluctuations have little impact on positions we intend to hold for several years or longer. Our short and medium term investments are the only positions affected by these daily and weekly fluctuations.

This commentary is for informational purposes and is not investment advice, an indicator of future performance, a solicitation, an offer to buy or sell, or a recommendation for any security. It should not be used as a primary basis for making investment decisions. Consider your own financial circumstances and goals carefully before investing. Past performance cannot guarantee results.