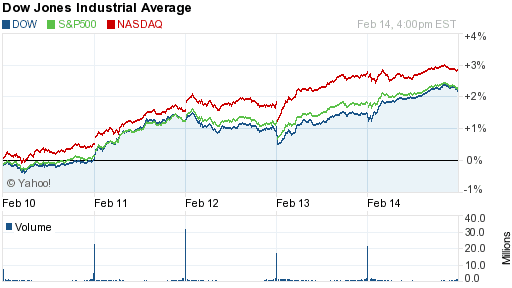

Stocks continued to rally this week, turning in their best performance of the year. Through the Friday close, the Dow and S&P both rose 2.3% while the Nasdaq was higher by 2.9%. Gold had a terrific week, climbing 4.4% to break out of the range it’s been stuck in the last several months. Oil continues to rise, too, up 0.4% to close at $100.30 per barrel. The international Brent crude moved higher to just above $109 per barrel.

Source: Yahoo Finance

The week was a very quiet one with little news affecting the market. Actually, there was more talk about the weather than anything else.

The cold weather and unusually large amount of snow affecting the country has many worried about its impact on the economy. Economists are already making downward revisions to their data forecasts and companies are warning of weaker sales. Regardless of it actually having any impact, the weather will provide an excuse for any poor economic report or corporate earnings over the next several weeks.

Blaming the weather is nothing new, really. Every season we hear the weather used as an excuse. If it’s too cold, people can’t go shop. If it’s too warm, not enough people bought jackets, which hurt earnings. You get the idea. This week it was cited as the reason for the worst decline in retail sales over the past year and a half and a decrease in industrial production.

While we’ll hear this excuse in the coming weeks, it will be difficult to determine its true impact on the economy, especially since the data has been deteriorating over the last several months.

While economic reports this week weren’t great, the first Congressional testimony of the new Fed chief gave stocks a reason to rise. As expected, Janet Yellen told us nothing new in expressing a desire to continue the policies of Ben Bernanke. It was what the market wanted to hear, though, since it doesn’t like change and does like the easy money policies of the Fed.

Stocks also appeared to get a boost from the extension of the debt ceiling until next year.

Finally, we’ll take a look at corporate earnings which have been particularly strong. According to Factset, earnings have grown a solid 8.3% while revenue (what the company made in sales. Revenue minus expenses gives us earnings) only grew at a 0.8% pace. Again, this shows how companies have been improving their bottom line not by increasing sales, but by cutting costs.

Interesting to note is that when announcing positive earnings, only 53% of companies’ stocks rose as a result. This is far below average. It shows us that investors are being pickier when looking at earnings and we’ll have to watch for how much impact it has on the broader market going forward.

Next Week

Next week looks to be a little busier, especially since we only have four trading days due to the Monday holiday. We’ll see reports on inflation, housing, and leading economic indicators. We’ll see some corporate earnings reports, too, but the amount of companies reporting continues to decline.

The Fed will also be in the news since several regional Fed presidents will be making speeches. Plus, the minutes from the last Fed meeting will be released.

Investment Strategy

Stocks have reversed course very sharply since their dismal opening to the year. We may not get another performance like we saw this week, but the market momentum is clearly higher. Being value investors by nature, we like buying on dips and wouldn’t put new money into the broader market at this point, but still see many undervalued individual names out there. .

As for bonds, yields continue to hover around these current levels and trying to figure out where they’ll go from here is a guessing game, at best. Bonds will always have their place in a portfolio, but there is a worry about rates rising (so prices would fall). A short position (bet on the decline in prices) acts as a nice hedge if yields do rise. Floating rate bonds are also gaining popularity for this same reason, but they tend to be riskier investments, so caution is warranted.

Continuing with bonds, TIPs remain an important hedge against future inflation and municipal bonds are in the same boat and work for the right client. We like buying individual, insured names for these bonds, avoiding muni index bonds if possible. We keep a longer term focus with these investments.

Gold reached its highest level in three months and finally broke through that $1,300 price level. It still looks volatile, but also acts as a good hedge in the longer run.

We like other commodities for the long term, especially due to weaker currencies around the globe. This is a longer-term play, so buying on the dips may work with a longer time horizon.

Finally, in international stocks, we see weakness around the globe and favor neither the developed or emerging markets.

Please note, these day-to-day and week-to-week fluctuations have little impact on positions we intend to hold for several years or longer. Our short and medium term investments are the only positions affected by these daily and weekly fluctuations.

This commentary is for informational purposes and is not investment advice, an indicator of future performance, a solicitation, an offer to buy or sell, or a recommendation for any security. It should not be used as a primary basis for making investment decisions. Consider your own financial circumstances and goals carefully before investing. Past performance cannot guarantee results.

The cold weather and unusually large amount of snow affecting the country has many worried about its impact on the economy. Economists are already making downward revisions to their data forecasts and companies are warning of weaker sales. Regardless of it actually having any impact, the weather will provide an excuse for any poor economic report or corporate earnings over the next several weeks.

Blaming the weather is nothing new, really. Every season we hear the weather used as an excuse. If it’s too cold, people can’t go shop. If it’s too warm, not enough people bought jackets, which hurt earnings. You get the idea. This week it was cited as the reason for the worst decline in retail sales over the past year and a half and a decrease in industrial production.

While we’ll hear this excuse in the coming weeks, it will be difficult to determine its true impact on the economy, especially since the data has been deteriorating over the last several months.

While economic reports this week weren’t great, the first Congressional testimony of the new Fed chief gave stocks a reason to rise. As expected, Janet Yellen told us nothing new in expressing a desire to continue the policies of Ben Bernanke. It was what the market wanted to hear, though, since it doesn’t like change and does like the easy money policies of the Fed.

Stocks also appeared to get a boost from the extension of the debt ceiling until next year.

Finally, we’ll take a look at corporate earnings which have been particularly strong. According to Factset, earnings have grown a solid 8.3% while revenue (what the company made in sales. Revenue minus expenses gives us earnings) only grew at a 0.8% pace. Again, this shows how companies have been improving their bottom line not by increasing sales, but by cutting costs.

Interesting to note is that when announcing positive earnings, only 53% of companies’ stocks rose as a result. This is far below average. It shows us that investors are being pickier when looking at earnings and we’ll have to watch for how much impact it has on the broader market going forward.

Next Week

Next week looks to be a little busier, especially since we only have four trading days due to the Monday holiday. We’ll see reports on inflation, housing, and leading economic indicators. We’ll see some corporate earnings reports, too, but the amount of companies reporting continues to decline.

The Fed will also be in the news since several regional Fed presidents will be making speeches. Plus, the minutes from the last Fed meeting will be released.

Investment Strategy

Stocks have reversed course very sharply since their dismal opening to the year. We may not get another performance like we saw this week, but the market momentum is clearly higher. Being value investors by nature, we like buying on dips and wouldn’t put new money into the broader market at this point, but still see many undervalued individual names out there. .

As for bonds, yields continue to hover around these current levels and trying to figure out where they’ll go from here is a guessing game, at best. Bonds will always have their place in a portfolio, but there is a worry about rates rising (so prices would fall). A short position (bet on the decline in prices) acts as a nice hedge if yields do rise. Floating rate bonds are also gaining popularity for this same reason, but they tend to be riskier investments, so caution is warranted.

Continuing with bonds, TIPs remain an important hedge against future inflation and municipal bonds are in the same boat and work for the right client. We like buying individual, insured names for these bonds, avoiding muni index bonds if possible. We keep a longer term focus with these investments.

Gold reached its highest level in three months and finally broke through that $1,300 price level. It still looks volatile, but also acts as a good hedge in the longer run.

We like other commodities for the long term, especially due to weaker currencies around the globe. This is a longer-term play, so buying on the dips may work with a longer time horizon.

Finally, in international stocks, we see weakness around the globe and favor neither the developed or emerging markets.

Please note, these day-to-day and week-to-week fluctuations have little impact on positions we intend to hold for several years or longer. Our short and medium term investments are the only positions affected by these daily and weekly fluctuations.

This commentary is for informational purposes and is not investment advice, an indicator of future performance, a solicitation, an offer to buy or sell, or a recommendation for any security. It should not be used as a primary basis for making investment decisions. Consider your own financial circumstances and goals carefully before investing. Past performance cannot guarantee results.