A gain in the market Friday pushed stocks into positive territory for the week. As of the close Friday, the Dow and S&P both rose 0.5% and the Nasdaq was higher by 0.6%. Gold was slightly higher, up 0.4%. Oil saw another loss this week, falling 6.5% to close at $44.20 per barrel. The international Brent oil lost a little more than $3 to close at $46.68.

Source: Google Finance

This week also marked an end to a very quiet month. Markets are often less active in the summer months as investors take vacations, etc., but this month was unusually quiet. Markets were only fractionally lower and traded in one of the narrowest trading ranges in decades.

That quiet trend continued this week. We saw modest moves in the markets and the volume of trades was very light. In fact, Monday had the lightest trading volume of the year.

With a possible interest rate hike from the Fed looming, investors have been cautious about making any big bets and being caught on the wrong side of the trade. This has made economic data very important, for positive reports could sway the Fed’s hand sooner rather than later.

This was the reason we saw very little action in the market until the big employment report on Friday. Investors didn’t want to make any large bets in case the data came in opposite of their expectations.

That quiet trend continued this week. We saw modest moves in the markets and the volume of trades was very light. In fact, Monday had the lightest trading volume of the year.

With a possible interest rate hike from the Fed looming, investors have been cautious about making any big bets and being caught on the wrong side of the trade. This has made economic data very important, for positive reports could sway the Fed’s hand sooner rather than later.

This was the reason we saw very little action in the market until the big employment report on Friday. Investors didn’t want to make any large bets in case the data came in opposite of their expectations.

The jobs report did come in below expectations. Economists were looking for a number close to 180,000 jobs added, only to see 151,000. As you can see in the nearby chart, this was well below the previous two months.

Though it was a disappointing number, it was a positive for the market. It decreased the chances of the Fed raising interest rates (the low rates have helped stocks rise) and stocks rose as a result.

Other economic data this week was mixed. Consumer incomes and spending were both higher while our manufacturing sector contracted over the previous month.

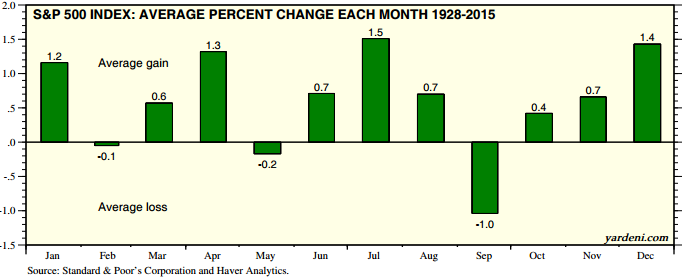

Finally, as we head into September, we should remember that the "Stock Trader's Almanac" reports that the month is historically the worst performer of the year. This is often attributed to investors starting to pay more attention to the market after the summer lull we discussed earlier. We’ll see if this dynamic play out again this year. Source: Ed Yardeni, S&P Corp, and Haver Analytics.

Though it was a disappointing number, it was a positive for the market. It decreased the chances of the Fed raising interest rates (the low rates have helped stocks rise) and stocks rose as a result.

Other economic data this week was mixed. Consumer incomes and spending were both higher while our manufacturing sector contracted over the previous month.

Finally, as we head into September, we should remember that the "Stock Trader's Almanac" reports that the month is historically the worst performer of the year. This is often attributed to investors starting to pay more attention to the market after the summer lull we discussed earlier. We’ll see if this dynamic play out again this year. Source: Ed Yardeni, S&P Corp, and Haver Analytics.

Next Week

Next week looks to be very quiet for market-moving data. There will be a report on the strength of the service sector, on employment, and the Fed’s beige book, which gives an anecdotal account of the strength of the economy. Plus, it’s a four-day week.

That said, the summertime lull usually wears off after Labor Day, so we may see volume start to pick up. That may bring us some more volatility.

Investment Strategy

No change here. Stocks are still on the “cheaper” side in the short run (a week to a few weeks). However, the direction of the market is still very dependent on Fed policy, so the likelihood for a change in policy will impact the market.

Looking out a little further, we see headwinds for stocks but the response from central banks will have the most influence on the direction of the market. Additional support, whether it is stimulus from printing money or lowering interest rates, will reassure the markets and likely see them head higher – or at least ease the decline.

In the long term we remain very cautious. The money printed through stimulus has masked many problems, causing a misallocation of resources and allowing bubbles to form. It prevented necessary changes from occurring at both a corporate and political level – changes that would actually help the economy. Just how far out this day of reckoning is remains anyone’s guess, however.

Bonds were again quiet this week as yields rose slightly (so prices fell slightly). We think prices will remain high and yields low, though, as demand from investors will continue to be strong.

Bonds to protect against inflation, or TIPs, remain a good long term hedge for inflation. Floating-rate bonds will do well if interest rates eventually do rise.

Some municipal bonds look attractive for the right client, too. We like buying individual, insured names for these bonds, avoiding muni index bonds if possible. We keep a longer term focus with these investments.

Gold is another good hedge for the portfolio. It is only a hedge at this point – rising on geopolitical issues as a flight to safety.

Finally, in international stocks, we see weakness around the globe and favor neither the developed or emerging markets.

Please note, these day-to-day and week-to-week fluctuations have little impact on positions we intend to hold for several years or longer. Our short and medium term investments are the only positions affected by these daily and weekly fluctuations.

This commentary is for informational purposes and is not investment advice, an indicator of future performance, a solicitation, an offer to buy or sell, or a recommendation for any security. It should not be used as a primary basis for making investment decisions. Consider your own financial circumstances and goals carefully before investing. Past performance cannot guarantee results.

Next week looks to be very quiet for market-moving data. There will be a report on the strength of the service sector, on employment, and the Fed’s beige book, which gives an anecdotal account of the strength of the economy. Plus, it’s a four-day week.

That said, the summertime lull usually wears off after Labor Day, so we may see volume start to pick up. That may bring us some more volatility.

Investment Strategy

No change here. Stocks are still on the “cheaper” side in the short run (a week to a few weeks). However, the direction of the market is still very dependent on Fed policy, so the likelihood for a change in policy will impact the market.

Looking out a little further, we see headwinds for stocks but the response from central banks will have the most influence on the direction of the market. Additional support, whether it is stimulus from printing money or lowering interest rates, will reassure the markets and likely see them head higher – or at least ease the decline.

In the long term we remain very cautious. The money printed through stimulus has masked many problems, causing a misallocation of resources and allowing bubbles to form. It prevented necessary changes from occurring at both a corporate and political level – changes that would actually help the economy. Just how far out this day of reckoning is remains anyone’s guess, however.

Bonds were again quiet this week as yields rose slightly (so prices fell slightly). We think prices will remain high and yields low, though, as demand from investors will continue to be strong.

Bonds to protect against inflation, or TIPs, remain a good long term hedge for inflation. Floating-rate bonds will do well if interest rates eventually do rise.

Some municipal bonds look attractive for the right client, too. We like buying individual, insured names for these bonds, avoiding muni index bonds if possible. We keep a longer term focus with these investments.

Gold is another good hedge for the portfolio. It is only a hedge at this point – rising on geopolitical issues as a flight to safety.

Finally, in international stocks, we see weakness around the globe and favor neither the developed or emerging markets.

Please note, these day-to-day and week-to-week fluctuations have little impact on positions we intend to hold for several years or longer. Our short and medium term investments are the only positions affected by these daily and weekly fluctuations.

This commentary is for informational purposes and is not investment advice, an indicator of future performance, a solicitation, an offer to buy or sell, or a recommendation for any security. It should not be used as a primary basis for making investment decisions. Consider your own financial circumstances and goals carefully before investing. Past performance cannot guarantee results.