The major markets were higher again this week, making this the eight-straight positive week for the Dow and S&P. Through the close Friday, the Dow rose 0.5%, the S&P gained 0.3%, and the Nasdaq added 0.9%. Bond prices turned the corner and rose this week as yields fell. Gold was off very slightly, down just 0.03%. Oil prices hit their highest level in two years, rising 3.4% this week to $55.70 per barrel. The international Brent oil moved higher to close at $62.09.

There was a lot of news in the market this week, but it didn’t translate to a lot of action for stocks.

The big story came Thursday as the long-awaited tax plan from House Republicans was released. Some of the headlines included a reduction in the corporate rate to 20%, while the individual side was slightly more complicated with a reduction in most tax brackets, a phase-out of the estate tax, and fewer tax deductions.

The big story came Thursday as the long-awaited tax plan from House Republicans was released. Some of the headlines included a reduction in the corporate rate to 20%, while the individual side was slightly more complicated with a reduction in most tax brackets, a phase-out of the estate tax, and fewer tax deductions.

In our view, the corporate side looks decent. Rumors early in the week suggested the reduction in the corporate rate would be phased in over a number of years. The news was not well received by the market and contributed to Monday’s selloff.

The tax plan for the individual side was disappointing. There is a reduction in rates, but many investors thought they might be lower. The phase-out of tax deductions also complicates the proposal and may make the plan difficult to pass in its current form.

The market did not see much reaction to the plan since many of the details were leaked prior to its announcement. However, several industries that would be negatively affected did see some action. Limits on mortgage interest and property tax deductions could have an effect on housing, and the homebuilder sector sold off strongly as a result. Likewise, an elimination of the credit for electric vehicles hit companies like Tesla.

The tax plan for the individual side was disappointing. There is a reduction in rates, but many investors thought they might be lower. The phase-out of tax deductions also complicates the proposal and may make the plan difficult to pass in its current form.

The market did not see much reaction to the plan since many of the details were leaked prior to its announcement. However, several industries that would be negatively affected did see some action. Limits on mortgage interest and property tax deductions could have an effect on housing, and the homebuilder sector sold off strongly as a result. Likewise, an elimination of the credit for electric vehicles hit companies like Tesla.

The other big story this week was the appointment of Jerome (or Jay) Powell to head the Federal Reserve. He was seen as the safe choice to follow Janet Yellen and will continue many of her policies – and the market likes continuity. He is also seen as being lighter on financial regulation, which is important after many years of increasing regulations.

The Fed also held a policy meeting this week where they left interest rates unchanged, as expected. However, they still appear to be on pact to raise rates in December.

Corporate earnings were also a big story this week. Just over 80% of companies in the S&P 500 have reported results thus far, so we have a pretty good idea of the earnings picture. The results have been decent, with earnings growing at a 5.9% pace, which is above the 4.2% analysts were predicting at the start of earnings season.

Finally, economic data released this week was largely positive.

The big report came on Friday with the release of October’s employment data. The economy added 261,000 jobs, which was lower than the 300,000+ many were expecting. However, the previous two months were revised higher by 90,000 jobs, which balances it out. Remember, last month showed a loss in jobs, but this number was revised to a positive number. It’s unusual to see such large misses and revisions, but the storms in the early fall has skewed this number.

The Fed also held a policy meeting this week where they left interest rates unchanged, as expected. However, they still appear to be on pact to raise rates in December.

Corporate earnings were also a big story this week. Just over 80% of companies in the S&P 500 have reported results thus far, so we have a pretty good idea of the earnings picture. The results have been decent, with earnings growing at a 5.9% pace, which is above the 4.2% analysts were predicting at the start of earnings season.

Finally, economic data released this week was largely positive.

The big report came on Friday with the release of October’s employment data. The economy added 261,000 jobs, which was lower than the 300,000+ many were expecting. However, the previous two months were revised higher by 90,000 jobs, which balances it out. Remember, last month showed a loss in jobs, but this number was revised to a positive number. It’s unusual to see such large misses and revisions, but the storms in the early fall has skewed this number.

As for other economic data, the strength of the manufacturing and service sectors was very high, worker productivity rose to its best level since 2014, factory orders were higher, and consumer confidence hit a 17-year high.

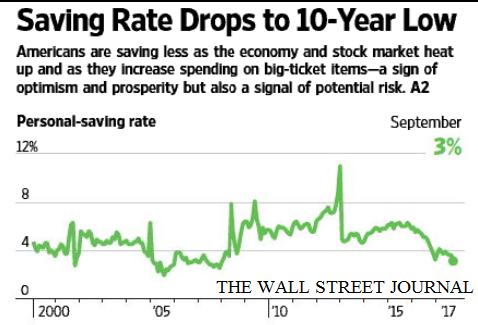

One interesting stat showed that the savings rate (the amount people save from each paycheck) dropped to a 10-year low. Many investors see this as a positive, since it means higher spending and is a sign of confidence in the future. We worry, though, that rainy days often come when you don’t prepare for them.

Next Week

We’re getting towards the end of corporate earnings season, but there will still be a number of reports out next week as about 10% of the S&P 500 reports results. Many media companies and retailers, in particular, will be reporting results. The week will be a very quiet one for economic data.

More work will be done on the tax plan and we’ll be watching to see how it shapes up.

Investment Strategy

No change here. We’ve been expecting to see a pause or decline in this market rally, but have clearly been wrong thus far. We still think the market is on the expensive side and hesitate to put new money into the broader indexes. However, there are many individual stocks that may be trading at attractive levels.

Below is an update to some of the leading indicators we follow. As the stock market rises, these indicators continue to move lower. This shows investors are taking less risk and the stock market is becoming more susceptible to a large correction. This is something to keep an eye on.

We’re getting towards the end of corporate earnings season, but there will still be a number of reports out next week as about 10% of the S&P 500 reports results. Many media companies and retailers, in particular, will be reporting results. The week will be a very quiet one for economic data.

More work will be done on the tax plan and we’ll be watching to see how it shapes up.

Investment Strategy

No change here. We’ve been expecting to see a pause or decline in this market rally, but have clearly been wrong thus far. We still think the market is on the expensive side and hesitate to put new money into the broader indexes. However, there are many individual stocks that may be trading at attractive levels.

Below is an update to some of the leading indicators we follow. As the stock market rises, these indicators continue to move lower. This shows investors are taking less risk and the stock market is becoming more susceptible to a large correction. This is something to keep an eye on.

Our longer term outlook remains positive, but less rosy than it was several months ago. We’re encouraged to see pro-business reforms coming out of Washington, although they are increasingly becoming watered-down. Additionally, companies have favored returning cash to shareholders through dividends and buybacks over the last several years and we believe the lack of reinvestment in their companies will weigh on earnings in the future.

Bond prices remain on the low side on a short-term basis and yields are on the higher. We don’t think yields have much room to move higher and think prices will firm up from here.

As for the rest of the portfolio, bonds to protect against inflation, or TIPs, remain a good long term hedge for inflation. Floating-rate bonds will do well if interest rates eventually do rise.

Some municipal bonds look attractive for the right client, too. We like buying individual, insured names for these bonds, avoiding muni index bonds if possible. We keep a longer term focus with these investments.

Gold is another good hedge for the portfolio. It is only a hedge at this point – rising on geopolitical issues as a flight to safety.

Finally, in international stocks, we see weakness around the globe and favor neither the developed or emerging markets, though they are looking cheap.

This commentary is for informational purposes and is not investment advice, an indicator of future performance, a solicitation, an offer to buy or sell, or a recommendation for any security. It should not be used as a primary basis for making investment decisions. Consider your own financial circumstances and goals carefully before investing. Past performance cannot guarantee results.

Bond prices remain on the low side on a short-term basis and yields are on the higher. We don’t think yields have much room to move higher and think prices will firm up from here.

As for the rest of the portfolio, bonds to protect against inflation, or TIPs, remain a good long term hedge for inflation. Floating-rate bonds will do well if interest rates eventually do rise.

Some municipal bonds look attractive for the right client, too. We like buying individual, insured names for these bonds, avoiding muni index bonds if possible. We keep a longer term focus with these investments.

Gold is another good hedge for the portfolio. It is only a hedge at this point – rising on geopolitical issues as a flight to safety.

Finally, in international stocks, we see weakness around the globe and favor neither the developed or emerging markets, though they are looking cheap.

This commentary is for informational purposes and is not investment advice, an indicator of future performance, a solicitation, an offer to buy or sell, or a recommendation for any security. It should not be used as a primary basis for making investment decisions. Consider your own financial circumstances and goals carefully before investing. Past performance cannot guarantee results.