It’s that time of year again. As you may be aware, our office is located at the entrance of TPC Sawgrass, home of the Players Championship. Tournament practice rounds begin Monday and we will be attending for much of the week. However, we will be in the office every day, though our hours will vary day-to-day. We will continue to monitor the market even though we may not be in the office. Any phone calls not immediately answered will be returned the same day. We foresee little to no inconvenience to our clients and hope for your understanding. There will be no market commentary next week. Thank you.

Stocks spent most of the week in negative territory though solid gains Friday erased some of the losses. For the week, the Dow and S&P were both down 0.2% while the Nasdaq was higher by 1.3%. Bonds saw little change on the week. Gold lost ground again, down 0.4%. Oil moved higher, up 2.5% to close at $69.79 per barrel. The international Brent oil, which is used for much of our gas here in the East, rose slightly to $75.00.

Stocks spent most of the week in negative territory though solid gains Friday erased some of the losses. For the week, the Dow and S&P were both down 0.2% while the Nasdaq was higher by 1.3%. Bonds saw little change on the week. Gold lost ground again, down 0.4%. Oil moved higher, up 2.5% to close at $69.79 per barrel. The international Brent oil, which is used for much of our gas here in the East, rose slightly to $75.00.

Stocks saw a lot of action this week, pushed and pulled by a variety of different stories. Market technicals played a part in some of the moves, but there was also news out on earnings, economic data, and the Fed that all had an impact.

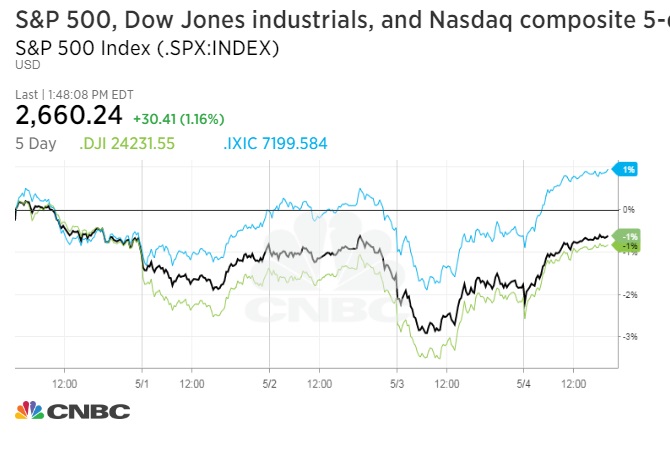

We don’t spend a lot of time talking about the technicals in this commentary (the technicals focus on the charts, where price and volume can indicate where an investment is likely to go), but they played an important part in the in the behavior of the market this week.

One widely-recognized technical indicator is the 200-day moving average, which is basically the average closing price over the last 200 days. This level can often act as a floor or a ceiling for stock or market prices.

As you can see in the chart below, this 200-day average is currently acting as a floor (or support) for market, where prices rarely go below this level. The market hit the 200-day average briefly Thursday and Friday before rebounding sharply both times.

We don’t spend a lot of time talking about the technicals in this commentary (the technicals focus on the charts, where price and volume can indicate where an investment is likely to go), but they played an important part in the in the behavior of the market this week.

One widely-recognized technical indicator is the 200-day moving average, which is basically the average closing price over the last 200 days. This level can often act as a floor or a ceiling for stock or market prices.

As you can see in the chart below, this 200-day average is currently acting as a floor (or support) for market, where prices rarely go below this level. The market hit the 200-day average briefly Thursday and Friday before rebounding sharply both times.

This week was also busy for news moving the market. We’ll start with corporate earnings, with just over half of the companies in the S&P 500 having reported results at this time.

The earnings numbers still look good – earnings have risen more than 20% and revenue (what a company earned through sales) rose roughly half that.

Much of the growth in earnings came from the corporate tax cut, which has been a big tailwind for companies. Growth in earnings still looks good if we take out that tax impact, too. According to Thompson Reuters, earnings have risen 12.1% on a pre-tax basis, which is solid.

Still, companies that have seen the biggest reduction in tax rates have outperformed those that already had a lower tax rate:

The earnings numbers still look good – earnings have risen more than 20% and revenue (what a company earned through sales) rose roughly half that.

Much of the growth in earnings came from the corporate tax cut, which has been a big tailwind for companies. Growth in earnings still looks good if we take out that tax impact, too. According to Thompson Reuters, earnings have risen 12.1% on a pre-tax basis, which is solid.

Still, companies that have seen the biggest reduction in tax rates have outperformed those that already had a lower tax rate:

There were several important economic reports released this week, too, and the results were disappointing.

The economy added 164,000 jobs last month, below the 190,000 expected.

The economy added 164,000 jobs last month, below the 190,000 expected.

However, the unemployment rate hit 3.9%, its lowest level in 17 years.

The strength of the manufacturing and service sectors also ticked lower over the last month. They still show growth, just at not as strong of a pace as before.

We also saw inflation tick higher according to the PCE inflation report (PCE stands for Personal Consumption Expenditure, which shows price changes in a fixed basket of items). The PCE is important because it is the primary inflation indicator the Fed looks at for determining policy. Inflation according to the PCE, inflation hit 2% over the past year, right at the level the Fed is targeting.

Speaking of the Fed, they held a meeting this week to discuss their economic policy. Investors have been worried that rising inflation and the growing economy would cause the Fed to further put the brakes on their economic stimulus policy. However, their comments this week suggested they were unlikely to do so.

The Fed placed an emphasis on the word “symmetric” when referring to inflation. Their target is 2% inflation, but as you can see in the chart below, inflation has been below that level for many years. By “symmetric,” they mean they want inflation to run above 2% for a while before they become aggressive in pulling back on stimulus.

Speaking of the Fed, they held a meeting this week to discuss their economic policy. Investors have been worried that rising inflation and the growing economy would cause the Fed to further put the brakes on their economic stimulus policy. However, their comments this week suggested they were unlikely to do so.

The Fed placed an emphasis on the word “symmetric” when referring to inflation. Their target is 2% inflation, but as you can see in the chart below, inflation has been below that level for many years. By “symmetric,” they mean they want inflation to run above 2% for a while before they become aggressive in pulling back on stimulus.

Frankly, we think their inflation target should be 0% as it was mandated by Congress. Rising inflation is harmful to consumers who have to pay more and more every year. High inflation only benefits those with high debt…like the government. Interesting how that works out.

Next Week

Next week will be another busy one. We’re on the back half of earnings season, but there will still be a large number of companies releasing their results. We’ll get another look at inflation with the CPI and PPI reports, plus small business optimism, and employment.

Investment Strategy

Stocks are looking more attractive after the selloff over the last few weeks. Prices need to move a little lower before they become a compelling buy, but they are near an interesting level. We think it is unlikely the Fed will aggressively tighten their policy, especially after their comments this week on inflation and the mediocre economic data, so this will also help stocks higher.

The longer term direction of the market is a little difficult to predict. Fundamentals remain very good with pro-business policies out of Washington providing a solid tailwind. However, rising interest rates (which are like Kryptonite to stocks) could pull markets lower. It’s tough to say where we think the market will go the long run.

Bonds are also volatile at this time. Yields have broken out higher in the last few weeks (so prices moved lower), but we think they are near the high end of their range right now.

As for the rest of the portfolio, bonds to protect against inflation, or TIPs, remain a good long term hedge for inflation. Floating-rate bonds will do well if interest rates do rise.

Some municipal bonds look attractive for the right client, too. We like buying individual, insured names for these bonds, avoiding muni index bonds if possible. We keep a longer term focus with these investments.

Gold is another good hedge for the portfolio. It is only a hedge at this point – rising on geopolitical issues as a flight to safety.

Finally, in international stocks, we prefer developed markets to emerging ones at this time.

This commentary is for informational purposes and is not investment advice, an indicator of future performance, a solicitation, an offer to buy or sell, or a recommendation for any security. It should not be used as a primary basis for making investment decisions. Consider your own financial circumstances and goals carefully before investing. Past performance cannot guarantee results.

Next Week

Next week will be another busy one. We’re on the back half of earnings season, but there will still be a large number of companies releasing their results. We’ll get another look at inflation with the CPI and PPI reports, plus small business optimism, and employment.

Investment Strategy

Stocks are looking more attractive after the selloff over the last few weeks. Prices need to move a little lower before they become a compelling buy, but they are near an interesting level. We think it is unlikely the Fed will aggressively tighten their policy, especially after their comments this week on inflation and the mediocre economic data, so this will also help stocks higher.

The longer term direction of the market is a little difficult to predict. Fundamentals remain very good with pro-business policies out of Washington providing a solid tailwind. However, rising interest rates (which are like Kryptonite to stocks) could pull markets lower. It’s tough to say where we think the market will go the long run.

Bonds are also volatile at this time. Yields have broken out higher in the last few weeks (so prices moved lower), but we think they are near the high end of their range right now.

As for the rest of the portfolio, bonds to protect against inflation, or TIPs, remain a good long term hedge for inflation. Floating-rate bonds will do well if interest rates do rise.

Some municipal bonds look attractive for the right client, too. We like buying individual, insured names for these bonds, avoiding muni index bonds if possible. We keep a longer term focus with these investments.

Gold is another good hedge for the portfolio. It is only a hedge at this point – rising on geopolitical issues as a flight to safety.

Finally, in international stocks, we prefer developed markets to emerging ones at this time.

This commentary is for informational purposes and is not investment advice, an indicator of future performance, a solicitation, an offer to buy or sell, or a recommendation for any security. It should not be used as a primary basis for making investment decisions. Consider your own financial circumstances and goals carefully before investing. Past performance cannot guarantee results.