Stocks turned in a solid week despite some speed bumps. Through Friday’s close, the Dow gained 2.3%, the S&P rose 1.5%, and the Nasdaq hit an all-time high with a 1.8% pop. Bonds prices saw little change. Gold keeps moving lower with a 1.0% drop this week. Oil prices fell too, losing 4.4% to close at $70.58 per barrel. The international Brent oil moved lower to close at $74.92.

The story in the stock market this week was the same as it’s been the last several weeks – stocks are moving higher on solid earnings and economic growth but takes a hit when trade tensions flare up.

Stocks were higher every day this week except one, when the Trump administration announced it would impose a 10% tariff on $200 billion of Chinese imports. These tariffs come after $50 billion was already implemented on Chinese goods, showing the trade war is clearly escalating.

However, the market quickly brushed it off after the initial selloff. The tariffs won’t take effect for two months at the earliest and there is hope that negotiations will work out a deal before they can be implemented.

While our stock market has fared well amid these escalating trade threats, the Chinese market has not. Their falling stock market strengthened our hand in the negotiations. However, it looks like their market may be finding a bottom.

Stocks were higher every day this week except one, when the Trump administration announced it would impose a 10% tariff on $200 billion of Chinese imports. These tariffs come after $50 billion was already implemented on Chinese goods, showing the trade war is clearly escalating.

However, the market quickly brushed it off after the initial selloff. The tariffs won’t take effect for two months at the earliest and there is hope that negotiations will work out a deal before they can be implemented.

While our stock market has fared well amid these escalating trade threats, the Chinese market has not. Their falling stock market strengthened our hand in the negotiations. However, it looks like their market may be finding a bottom.

These trade wars are also weighing on economic growth forecasts – both here and abroad.

There are several markets investors can look at to get an idea on the strength of the global economy. One is copper. Copper is used in all sorts of ways – in homes and buildings with copper pipes and wiring to electronics and other industrial uses. Its widespread use generally correlates to an economy – more copper use indicates a growing economy and vice versa.

As we can see in the chart below, though, copper prices are falling. This suggests worries that economic growth around the world is slowing and is something to keep an eye on.

There are several markets investors can look at to get an idea on the strength of the global economy. One is copper. Copper is used in all sorts of ways – in homes and buildings with copper pipes and wiring to electronics and other industrial uses. Its widespread use generally correlates to an economy – more copper use indicates a growing economy and vice versa.

As we can see in the chart below, though, copper prices are falling. This suggests worries that economic growth around the world is slowing and is something to keep an eye on.

Staying with the economy theme, economic reports released this week were mixed.

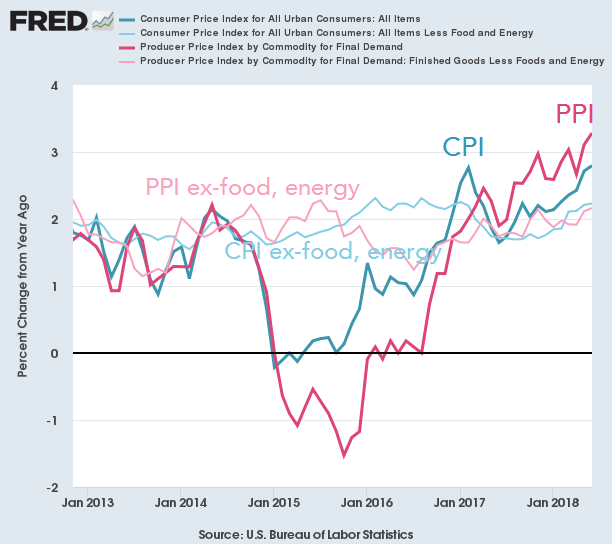

The big report of the week was inflation, which is really picking up. Inflation at the consumer level rose 2.9% over the past year, the highest level since 2012. Inflation at the producer level rose 3.4%, its highest since 2011. Rising inflation is likely to cause the Fed to keep pulling back on its stimulus program.

The big report of the week was inflation, which is really picking up. Inflation at the consumer level rose 2.9% over the past year, the highest level since 2012. Inflation at the producer level rose 3.4%, its highest since 2011. Rising inflation is likely to cause the Fed to keep pulling back on its stimulus program.

On the positive side, the employment picture looks solid and there are more jobs available then there are unemployed people. That means in a perfect world where there was a match between workers and employers, there would be no unemployed people.

Also, small business optimism ticked slightly lower this week but remains at a very high level.

Lastly, corporate earnings for the second quarter started rolling in with a few big banks reporting results. Next week the pace will pick up, which will be nice to draw some of the media attention away from trade fights.

Earnings are estimated to grow 20% over the past year according to Factset. This is a solid number, but investors see this as a slowdown since earnings rose 26% last quarter. Nonetheless, earnings still look strong.

Next Week

Next week looks to be a little busier. Trade concerns will still stay with us, but we’ll also see corporate earnings reports picking up and get a few important economic data points, including retail sales and industrial production. The Fed will also be in the news as Fed chairman Powell appears before congress.

Investment Strategy

Stocks no longer look cheap to us on a short term basis and we would hesitate to put new money here. While the odds of a pause or pullback have risen, stocks still appear to have the wind at their back and we aren’t overly concerned with a large decline at this time.

There is no change in our longer term forecast, which remains difficult to predict. Fundamentals are still very good with pro-business policies out of Washington providing a solid tailwind. However, rising interest rates have historically pulled markets lower. It’s tough to say where we think the market will go the long run.

Bonds are also volatile at this time. Yields have come off their recent highs (and prices off their recent lows) and we think they will continue to trade in this range for the foreseeable future.

As for the rest of the portfolio, bonds to protect against inflation, or TIPs, remain a good long term hedge for inflation. Floating-rate bonds will do well if interest rates do rise.

Some municipal bonds look attractive for the right client, too. We like buying individual, insured names for these bonds, avoiding muni index bonds if possible. We keep a longer term focus with these investments.

Gold is another good hedge for the portfolio. It is only a hedge at this point – rising on geopolitical issues as a flight to safety.

Finally, in international stocks, we prefer developed markets to emerging ones at this time.

This commentary is for informational purposes and is not investment advice, an indicator of future performance, a solicitation, an offer to buy or sell, or a recommendation for any security. It should not be used as a primary basis for making investment decisions. Consider your own financial circumstances and goals carefully before investing. Past performance cannot guarantee results.

Earnings are estimated to grow 20% over the past year according to Factset. This is a solid number, but investors see this as a slowdown since earnings rose 26% last quarter. Nonetheless, earnings still look strong.

Next Week

Next week looks to be a little busier. Trade concerns will still stay with us, but we’ll also see corporate earnings reports picking up and get a few important economic data points, including retail sales and industrial production. The Fed will also be in the news as Fed chairman Powell appears before congress.

Investment Strategy

Stocks no longer look cheap to us on a short term basis and we would hesitate to put new money here. While the odds of a pause or pullback have risen, stocks still appear to have the wind at their back and we aren’t overly concerned with a large decline at this time.

There is no change in our longer term forecast, which remains difficult to predict. Fundamentals are still very good with pro-business policies out of Washington providing a solid tailwind. However, rising interest rates have historically pulled markets lower. It’s tough to say where we think the market will go the long run.

Bonds are also volatile at this time. Yields have come off their recent highs (and prices off their recent lows) and we think they will continue to trade in this range for the foreseeable future.

As for the rest of the portfolio, bonds to protect against inflation, or TIPs, remain a good long term hedge for inflation. Floating-rate bonds will do well if interest rates do rise.

Some municipal bonds look attractive for the right client, too. We like buying individual, insured names for these bonds, avoiding muni index bonds if possible. We keep a longer term focus with these investments.

Gold is another good hedge for the portfolio. It is only a hedge at this point – rising on geopolitical issues as a flight to safety.

Finally, in international stocks, we prefer developed markets to emerging ones at this time.

This commentary is for informational purposes and is not investment advice, an indicator of future performance, a solicitation, an offer to buy or sell, or a recommendation for any security. It should not be used as a primary basis for making investment decisions. Consider your own financial circumstances and goals carefully before investing. Past performance cannot guarantee results.