The markets closed out the quarter on a sour note. For the week, the Dow fell 1.1%, the S&P was lower by 1.3%, and the Nasdaq returned -2.0%. The results for the quarter were much better, with the Dow higher by 4.3%, the S&P rose 5.8%, and the Nasdaq turned in a nice gain of 6.2%. For commodities, gold was slightly lower by 0.3% this week. Oil bounced around, but closed down 0.8%. The other major type of oil, Brent, closed above $112 per barrel.

Source: MSN Moneycentral

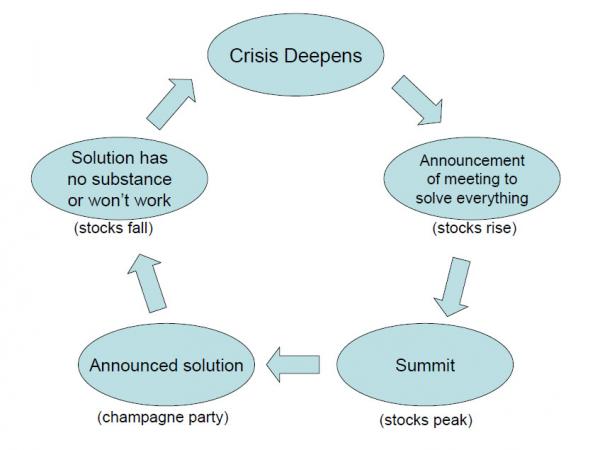

Problems in Europe resurfaced this week, contributing to the negative performance of the market. Doubts on the effectiveness of the recent stimulus and sour economic data also added to the downward pressure.

Thinking back to our commentary last week, we mentioned a news article (LINK) that highlighted the “agreement” between our President and European leaders for no surprises from that region before the election. As this week has shown, that doesn’t appear to be working.

In order to be eligible for bailout funds, a country must show an effort towards reducing their deficits. This week, Spain and Greece announced new austerity measures of additional tax hikes and spending cuts to again meet that requirement.

That did not sit well with the populace who took to the streets in protest. Spain, in particular, saw very large gatherings of protestors.

The hostile images lead many to wonder if the new tax hikes and spending cuts would actually be implemented. That would result in a loss of the necessary bailout funds, a worry that sent the markets lower.

Interestingly enough, some austerity measures have already been implemented in Spain, with tax increases and spending cuts already in place. Yet we learned this week that spending has risen 8.9% so far this year, while tax receipts were lower by 4.6%.

Remember, increased taxes have shown to stifle economic growth. And that slower growth leads to less tax revenue collected by the government. The optimal combination is lower government spending combined with lower taxes. Until reforms along those lines are made, the disappointing results are no surprise and will continue.

Adding to the negative pressure of the market, a Fed official threw cold water on the latest round of stimulus. Philadelphia Fed President Plosser made news by saying he didn’t think the latest stimulus will improve the economy or boost growth. He also was concerned that this bond buying would hurt the Fed’s credibility. The comments were unexpected and helped send the markets lower.

As for economic data this week, the results were mixed, though leaned to the negative side.

For the positives, consumer confidence was strong and home prices have risen. Personal income showed a slight gain (though is negative when considering inflation). Plus, the employment picture looked a little brighter this week.

On the negative side, new home sales came in below estimates. Manufacturing in the Chicago region showed a contraction for the first time since 2009. Durable goods showed a substantial drop of 13.1%. Most importantly, the final revision to the second quarter GDP showed a growth of only 1.3% (1.25%, actually), revised down from 1.7%. Unfortunately, economic growth has steadily declined over the past year and the trend is headed lower.

Next week

With the month and quarter ending this week, next week will be busier due to the economic information that will be released. Of note, we will get info on the strength of the manufacturing and service sectors, auto sales, and the important monthly employment report. Company earnings will also begin trickling in.

Fed Chairman Bernanke will be speaking next week, as well. Since the market is currently more focused on stimulus and bailouts than fundamentals like earnings and economic growth, Bernanke’s comments will be closely scrutinized.

Investment Strategy

The week was another disappointment after the big stimulus announcement two weeks ago. Past stimulus programs saw a corresponding rise in the market and that has yet to be the case here. While most see a good chance the market will rise once the stimulus gets into gear, caution is still warranted. As these weeks have shown, the market usually does the opposite of what most think it will.

If we do see a buying opportunity, in stocks, we still like large cap higher-quality and dividend paying stocks. Smaller and little-known stocks with low correlation to the market (and Europe) are also promising. There is always the opportunity to find an undervalued individual stock at any time, as well.

Gold is a longer-term favorite, as it will do well with the global money printing, additional bailouts, and stimulus programs. We wouldn’t add to positions at this point, but would not look to sell, either.

We like other commodities for the long term and had feared a slowdown in China and the other BRIC countries (Brazil, Russia, and India), pushing commodity prices lower in the short run. However, the recent stimulus may send this sector higher and prices may rise from here.

Treasury bonds yields have moved off their historic lows (where prices were near historic highs), as the new stimulus program shifted its attention from these bonds towards mortgage bonds. We wouldn’t consider the trend to be changing, for a continuation of the current Operation Twist (that has kept Treasury yields low and prices high and is set to expire at the end of the year) is likely. A short position (bet on a decline in price) provides a nice hedge here but we believe the potential for profit is low at this time.

On the bond theme, we think TIPs are important as we still expect inflation to increase. Municipal bonds also work and there are some nice yielding bonds out there now (try to avoid muni funds and buy the actual bond if possible), though our concern has increased as the pace of distressed municipalities is increasing. Additionally, higher taxes from the health care law will increase the attractiveness of these bonds in the future.

Finally, in international stocks, we favor developed international markets as opposed to emerging.

These day-to-day and week-to-week fluctuations have little impact on positions we intend to hold for several years or longer. Our short and medium term investments are the only positions affected by these daily and weekly fluctuations.

This commentary is for informational purposes and is not investment advice, an indicator of future performance, a solicitation, an offer to buy or sell, or a recommendation for any security. It should not be used as a primary basis for making investment decisions. Consider your own financial circumstances and goals carefully before investing. Past performance cannot guarantee results.

Thinking back to our commentary last week, we mentioned a news article (LINK) that highlighted the “agreement” between our President and European leaders for no surprises from that region before the election. As this week has shown, that doesn’t appear to be working.

In order to be eligible for bailout funds, a country must show an effort towards reducing their deficits. This week, Spain and Greece announced new austerity measures of additional tax hikes and spending cuts to again meet that requirement.

That did not sit well with the populace who took to the streets in protest. Spain, in particular, saw very large gatherings of protestors.

The hostile images lead many to wonder if the new tax hikes and spending cuts would actually be implemented. That would result in a loss of the necessary bailout funds, a worry that sent the markets lower.

Interestingly enough, some austerity measures have already been implemented in Spain, with tax increases and spending cuts already in place. Yet we learned this week that spending has risen 8.9% so far this year, while tax receipts were lower by 4.6%.

Remember, increased taxes have shown to stifle economic growth. And that slower growth leads to less tax revenue collected by the government. The optimal combination is lower government spending combined with lower taxes. Until reforms along those lines are made, the disappointing results are no surprise and will continue.

Adding to the negative pressure of the market, a Fed official threw cold water on the latest round of stimulus. Philadelphia Fed President Plosser made news by saying he didn’t think the latest stimulus will improve the economy or boost growth. He also was concerned that this bond buying would hurt the Fed’s credibility. The comments were unexpected and helped send the markets lower.

As for economic data this week, the results were mixed, though leaned to the negative side.

For the positives, consumer confidence was strong and home prices have risen. Personal income showed a slight gain (though is negative when considering inflation). Plus, the employment picture looked a little brighter this week.

On the negative side, new home sales came in below estimates. Manufacturing in the Chicago region showed a contraction for the first time since 2009. Durable goods showed a substantial drop of 13.1%. Most importantly, the final revision to the second quarter GDP showed a growth of only 1.3% (1.25%, actually), revised down from 1.7%. Unfortunately, economic growth has steadily declined over the past year and the trend is headed lower.

Next week

With the month and quarter ending this week, next week will be busier due to the economic information that will be released. Of note, we will get info on the strength of the manufacturing and service sectors, auto sales, and the important monthly employment report. Company earnings will also begin trickling in.

Fed Chairman Bernanke will be speaking next week, as well. Since the market is currently more focused on stimulus and bailouts than fundamentals like earnings and economic growth, Bernanke’s comments will be closely scrutinized.

Investment Strategy

The week was another disappointment after the big stimulus announcement two weeks ago. Past stimulus programs saw a corresponding rise in the market and that has yet to be the case here. While most see a good chance the market will rise once the stimulus gets into gear, caution is still warranted. As these weeks have shown, the market usually does the opposite of what most think it will.

If we do see a buying opportunity, in stocks, we still like large cap higher-quality and dividend paying stocks. Smaller and little-known stocks with low correlation to the market (and Europe) are also promising. There is always the opportunity to find an undervalued individual stock at any time, as well.

Gold is a longer-term favorite, as it will do well with the global money printing, additional bailouts, and stimulus programs. We wouldn’t add to positions at this point, but would not look to sell, either.

We like other commodities for the long term and had feared a slowdown in China and the other BRIC countries (Brazil, Russia, and India), pushing commodity prices lower in the short run. However, the recent stimulus may send this sector higher and prices may rise from here.

Treasury bonds yields have moved off their historic lows (where prices were near historic highs), as the new stimulus program shifted its attention from these bonds towards mortgage bonds. We wouldn’t consider the trend to be changing, for a continuation of the current Operation Twist (that has kept Treasury yields low and prices high and is set to expire at the end of the year) is likely. A short position (bet on a decline in price) provides a nice hedge here but we believe the potential for profit is low at this time.

On the bond theme, we think TIPs are important as we still expect inflation to increase. Municipal bonds also work and there are some nice yielding bonds out there now (try to avoid muni funds and buy the actual bond if possible), though our concern has increased as the pace of distressed municipalities is increasing. Additionally, higher taxes from the health care law will increase the attractiveness of these bonds in the future.

Finally, in international stocks, we favor developed international markets as opposed to emerging.

These day-to-day and week-to-week fluctuations have little impact on positions we intend to hold for several years or longer. Our short and medium term investments are the only positions affected by these daily and weekly fluctuations.

This commentary is for informational purposes and is not investment advice, an indicator of future performance, a solicitation, an offer to buy or sell, or a recommendation for any security. It should not be used as a primary basis for making investment decisions. Consider your own financial circumstances and goals carefully before investing. Past performance cannot guarantee results.