Hello all – we hope you had a nice July.

The market returns this month were fairly decent, where they started off strong though they stalled in the latter half. For the month, the Dow rose 2.3%, the S&P gained 4.5%, and the Nasdaq, which has a higher concentration of tech companies, was higher by 4.3%.

The market returns this month were fairly decent, where they started off strong though they stalled in the latter half. For the month, the Dow rose 2.3%, the S&P gained 4.5%, and the Nasdaq, which has a higher concentration of tech companies, was higher by 4.3%.

There were a few other stories in the markets worth noting.

Gold and the dollar and their relationship grabbed headlines this month. Gold reached record highs…

Gold and the dollar and their relationship grabbed headlines this month. Gold reached record highs…

…while the dollar dropped sharply.

Part of this move can be attributed to investors’ concerns with the Fed’s stimulus programs, where they are printing seemingly infinite amounts of money to finance massive debt levels. If they are printing more dollars, it means the dollars will be worth less. That’s good for commodities, like gold. This has the potential to end very badly, but we don’t appear to be anywhere near that level yet.

We look at the move in these two as a vote of confidence in the economic policy. A weaker dollar and higher gold tells us there isn’t a lot of confidence at this time.

The Coronavirus was again the main topic this month. The amount of cases rose, which caused some volatility in the markets. More cases meant more shutdowns and we’re already starting to see a negative impact on economic data.

The latest surge appears to be peaking, though, and hopefully will continue to trend lower from here.

We look at the move in these two as a vote of confidence in the economic policy. A weaker dollar and higher gold tells us there isn’t a lot of confidence at this time.

____

The Coronavirus was again the main topic this month. The amount of cases rose, which caused some volatility in the markets. More cases meant more shutdowns and we’re already starting to see a negative impact on economic data.

The latest surge appears to be peaking, though, and hopefully will continue to trend lower from here.

Corporate earnings were a big story this month as the results for the second quarter started rolling in. So far, a little more than half of the companies in the S&P 500 have reported results and they have been better than expected.

Analysts expected to see a 44% decline in earnings over the past year, but the result has been only a 41% decline. Estimates usually don’t miss by this much, but the difference is more of a reflection on how hard it is to make predictions in this current environment.

Also, such a large decline is not really something to get excited about, but its not unexpected when an entire economy is shut down.

The earnings news wasn’t all bad, though, as many companies are seeing improving trends and raising their predictions for the future.

Analysts expected to see a 44% decline in earnings over the past year, but the result has been only a 41% decline. Estimates usually don’t miss by this much, but the difference is more of a reflection on how hard it is to make predictions in this current environment.

Also, such a large decline is not really something to get excited about, but its not unexpected when an entire economy is shut down.

The earnings news wasn’t all bad, though, as many companies are seeing improving trends and raising their predictions for the future.

____

Economic data released this month was a mixed bag. Data covering the second quarter was horrible, data for the month of June (and released this month) was decent, and recent data for July shows a clear stalling.

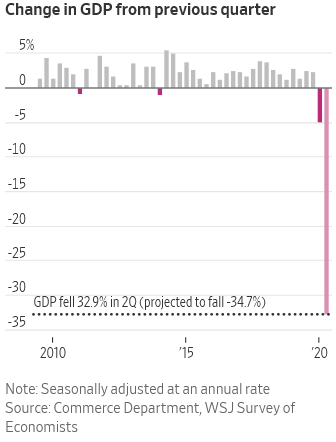

We’ll start with GDP for the second quarter, which was terrible. GDP, which measures the strength of the economy, fell by 34.7% over the past year.

This is the worst print for GDP - ever. Here’s a chart showing a longer view:

Despite the historic GDP decline, the results generated very little reaction in the markets. Investors knew the number would be bad since it covered the very darkest part of the shutdown. However, we know the economy has reopened at least partially since then and it’s likely we are past the worst of the virus.

In fact, estimates for next quarter’s GDP look solid:

In fact, estimates for next quarter’s GDP look solid:

As for other economic data released this month, the results were encouraging.

The strength of the manufacturing and service sectors rebounded sharply:

The strength of the manufacturing and service sectors rebounded sharply:

Retail sales have also sprung back:

Durable goods (which are items with a longer life, like a phone or refrigerator) look strong, as well.

However, we have to keep in mind that these reports did not include the last few weeks of July, where Coronavirus cases picked up and more shutdowns were imposed.

The weekly employment figures showed more people filing for unemployment over the last two weeks:

The weekly employment figures showed more people filing for unemployment over the last two weeks:

We’re also seeing one of our favorite leading indicators for the economy - the amount of people dining out - starting to stall.

While we are clearly doing better than a few months ago, the economy does appear to be stalling. Additional or prolonged shutdowns will continue to weigh on the economy and are likely to weigh on the markets, too.

As we near the Presidential election, it’s worth noting that the markets are a great indicator of who will win.

In the three months leading up to the election, a higher market is an indicator that the incumbent will win and a lower market signals an incumbent loss. This has been true every time since 1984 and 87% of the time since 1928. That’s a pretty solid track record!

____

As we near the Presidential election, it’s worth noting that the markets are a great indicator of who will win.

In the three months leading up to the election, a higher market is an indicator that the incumbent will win and a lower market signals an incumbent loss. This has been true every time since 1984 and 87% of the time since 1928. That’s a pretty solid track record!

____

Where does the market go from here?

Stocks are on the expensive side right now in the very short term. We aren’t predicting a downturn and the markets may even keep rising from here, but the odds of a decline have risen. Investors are very optimistic and it’s very cheap to hedge a portfolio, so maybe some downside protection is wise here.

The Corona cases remain the key - rising cases and further shutdowns will weigh on the markets. But the opposite is true, too. However, we think it’s unlikely the press will let the hype down before the election. There’s the potential for a lot of bad news out there, real or not.

This commentary is for informational purposes and is not investment advice, an indicator of future performance, a solicitation, an offer to buy or sell, or a recommendation for any security. It should not be used as a primary basis for making investment decisions. Consider your own financial circumstances and goals carefully before investing. Past performance cannot guarantee results.