Markets saw a lot of movement this week, closing with modest gains. For the week, the Dow was higher by 0.2%, the S&P rose 0.3%, and the Nasdaq returned 1.1%. Bond yields moved off their highest level since 2011 as their prices rose. Gold finally turned higher after trending lower since April, rising 0.9% this week. Oil reversed course, too, declining from its highest level since 2014. It lost 5.3% this week to close at $67.50 per barrel. The international Brent oil, which is used for much of our gas here in the East, closed down to $76.33.

There was very little economic data or corporate earnings reports to move markets this week. Instead, stocks moved sharply on geopolitical headlines North Korea and China received a lot of attention

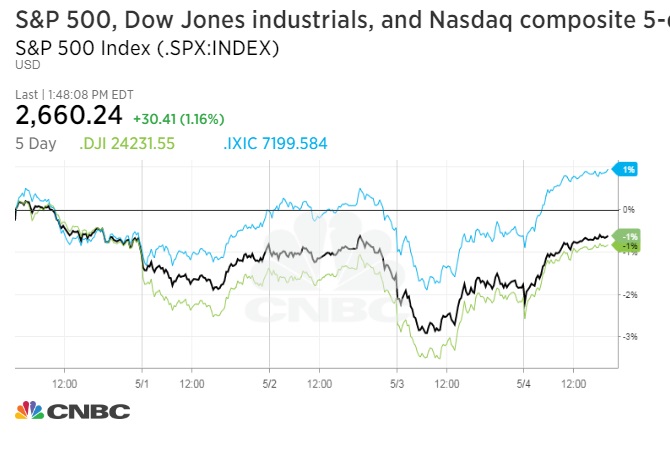

The chart below shows the market reacting to the various headlines this week:

The chart below shows the market reacting to the various headlines this week:

Stocks opened the week on a positive note as fears of a trade war with China eased over the weekend. Proposed tariffs were put on hold while trade negotiations continued.

It looked like progress on trade was being made, too. The U.S. planned to ease sanctions on Chinese telecom company ZTE for their violations while the Chinese agreed to buy more agricultural products and lowered the duties for autos coming in to their country.

Unfortunately the good news didn’t last long.

Tuesday afternoon, President Trump hinted that the summit with North Korea scheduled for June 12 might not happen. Stocks moved lower on the comments and continued lower into Wednesday.

By Thursday morning, President Trump announced the summit was cancelled, causing stocks to again fall.

While a possible resolution in the North Korean drama would be great for the world, the stock market is looking at this more in the terms of trade with China.

China’s influence on North Korea cannot be overstated and this was being used as a part of the trade negotiations with China. The U.S. had softened its tone on trade with China in exchange for their help in bringing North Korea to the table. Now that the summit is off, there is a worry that the U.S. may again take a hard line with China.

It wasn’t all bad news this week, as the minutes from the Fed’s latest meeting helped give stocks a boost.

The minutes showed that the Fed is very likely to pull pack further on their stimulus by raising interest rates at their next meeting (higher interest rates would make it more expensive to borrow money). However, the pace of any future increases in rates looks to be moderate.

It looked like progress on trade was being made, too. The U.S. planned to ease sanctions on Chinese telecom company ZTE for their violations while the Chinese agreed to buy more agricultural products and lowered the duties for autos coming in to their country.

Unfortunately the good news didn’t last long.

Tuesday afternoon, President Trump hinted that the summit with North Korea scheduled for June 12 might not happen. Stocks moved lower on the comments and continued lower into Wednesday.

By Thursday morning, President Trump announced the summit was cancelled, causing stocks to again fall.

While a possible resolution in the North Korean drama would be great for the world, the stock market is looking at this more in the terms of trade with China.

China’s influence on North Korea cannot be overstated and this was being used as a part of the trade negotiations with China. The U.S. had softened its tone on trade with China in exchange for their help in bringing North Korea to the table. Now that the summit is off, there is a worry that the U.S. may again take a hard line with China.

It wasn’t all bad news this week, as the minutes from the Fed’s latest meeting helped give stocks a boost.

The minutes showed that the Fed is very likely to pull pack further on their stimulus by raising interest rates at their next meeting (higher interest rates would make it more expensive to borrow money). However, the pace of any future increases in rates looks to be moderate.

As you can see in the chart below, the odds of a fourth rate hike this year dropped sharply:

Lastly, economic data released this week was light, though the reports released were on the disappointing side. Sales of durable goods, which are items that have a longer life span, fell from the previous month. Additionally, the pace of housing sales also declined from the previous month. This may reflect the higher mortgage rates that make it more expensive to purchase a home.

Next Week

A new month begins next week, which means we’ll start getting economic data for May. The big report comes on Friday with the monthly employment report and we’ll also get info on the strength of the manufacturing sector. The Fed will also release its Beige Book report, which gives an anecdotal look at the strength of the economy.

Investment Strategy

No change here. Stocks are still on the expensive side in the short term. That doesn’t mean we think they are going to fall, just that the odds of a decline are higher than a rise. We would be cautious about adding new money here.

The longer term direction of the market remains difficult to predict. Fundamentals are still very good with pro-business policies out of Washington providing a solid tailwind. However, rising interest rates are like Kryptonite to stocks and could pull markets lower. It’s tough to say where we think the market will go the long run.

Bonds are also volatile at this time. Yields have broken out higher in the last few weeks (so prices moved lower), but we think they are near the high end of their range right now.

As for the rest of the portfolio, bonds to protect against inflation, or TIPs, remain a good long term hedge for inflation. Floating-rate bonds will do well if interest rates do rise.

Some municipal bonds look attractive for the right client, too. We like buying individual, insured names for these bonds, avoiding muni index bonds if possible. We keep a longer term focus with these investments.

Gold is another good hedge for the portfolio. It is only a hedge at this point – rising on geopolitical issues as a flight to safety.

Finally, in international stocks, we prefer developed markets to emerging ones at this time.

This commentary is for informational purposes and is not investment advice, an indicator of future performance, a solicitation, an offer to buy or sell, or a recommendation for any security. It should not be used as a primary basis for making investment decisions. Consider your own financial circumstances and goals carefully before investing. Past performance cannot guarantee results.

A new month begins next week, which means we’ll start getting economic data for May. The big report comes on Friday with the monthly employment report and we’ll also get info on the strength of the manufacturing sector. The Fed will also release its Beige Book report, which gives an anecdotal look at the strength of the economy.

Investment Strategy

No change here. Stocks are still on the expensive side in the short term. That doesn’t mean we think they are going to fall, just that the odds of a decline are higher than a rise. We would be cautious about adding new money here.

The longer term direction of the market remains difficult to predict. Fundamentals are still very good with pro-business policies out of Washington providing a solid tailwind. However, rising interest rates are like Kryptonite to stocks and could pull markets lower. It’s tough to say where we think the market will go the long run.

Bonds are also volatile at this time. Yields have broken out higher in the last few weeks (so prices moved lower), but we think they are near the high end of their range right now.

As for the rest of the portfolio, bonds to protect against inflation, or TIPs, remain a good long term hedge for inflation. Floating-rate bonds will do well if interest rates do rise.

Some municipal bonds look attractive for the right client, too. We like buying individual, insured names for these bonds, avoiding muni index bonds if possible. We keep a longer term focus with these investments.

Gold is another good hedge for the portfolio. It is only a hedge at this point – rising on geopolitical issues as a flight to safety.

Finally, in international stocks, we prefer developed markets to emerging ones at this time.

This commentary is for informational purposes and is not investment advice, an indicator of future performance, a solicitation, an offer to buy or sell, or a recommendation for any security. It should not be used as a primary basis for making investment decisions. Consider your own financial circumstances and goals carefully before investing. Past performance cannot guarantee results.