The markets were more active this week, but the result was another flat market. Over the four-day week, the Dow was slightly higher by 0.1%, the S&P down by 0.3% for its first negative week of the year, and the Nasdaq lost 1.0%. The pain continued for gold as it sold off 2.3% to reach a seven-month low. Oil also dropped sharply, falling 3.4% to $93 per barrel. The international Brent oil closed down to $114. This may relieve some of the pressure at the pump, but issues with refineries are likely to hold gas prices higher.

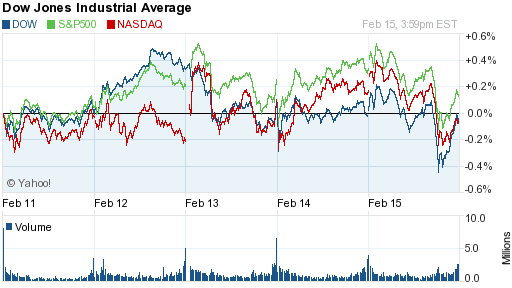

Source: Yahoo Finance (we were unable to adjust the chart for the Monday holiday)

Stocks started the week out on a fairly positive note. The markets crept higher, with the Dow just 1% from its all-time high. The VIX index (which measures volatility and is often referred to as the “fear gauge”) stood at its lowest level since 2007 (which meant fear was low).

Like Icarus flying too close to the sun, the markets plunged Wednesday and Thursday for the biggest two-day drop of the year. The VIX had its worst two-day stretch in 14 months (signaling volatility and fear increasing).

To this point in the rally, much of the negative news has been overlooked. After the run it has had, though, some investors (like us) have been getting jittery and looking for an excuse to take some money off the table. Some bad news this week provided that opportunity.

On Wednesday, the Fed released the minutes of its most recent meeting in January. There appeared to be a growing concern with some Fed members that the stimulus program is causing new risks in the economy. The cheap money could cause “economic and financial imbalances” according to one Fed member. This raised the idea that the asset purchases (money printing) could be scaled back from its $85 billion a month.

The idea that the Fed may not be as committed to its stimulus program sparked the strong sell-off in the market (while reaffirming that the market gains have been fueled by the Feds actions). Other negative economic data showing a drop in manufacturing in the Philadelphia region and a gain in weekly jobless claims added to the downward pressure.

By Friday, the market reversed course for a strong gain. Part of the reason for the rise may have been an appearance by one Fed member, James Bullard, on a CNBC morning program.

He stated that the Fed will stay “very aggressive…for a very long time.” That means the markets were wrong to be worried about the Fed earlier in the week and stimulus will continue, well, for a very long time. He also noted that the program in place since the beginning of the new year was more potent, since it is outright printing of $85 billion a month (once a phenomenally large number that barely elicits a response these days).

The market moved higher on the prospect of more money printing for a very long time (and again reaffirms that the market gains are fueled by the Feds actions).

One concern of these Fed programs has been inflation. Inflation reports released this week, the CPI and PPI, showed little to no gain in inflation over the month of January. The level remains well below the inflation target the Fed would like to see.

As anyone in the real world can attest to (as well as professionals who dig into the nuances of its calculation), the inflation results are laughable. According to shadowstats.com, if inflation today were to be measured using 1990 methodology, inflation would be running closer to 5%. Under 1980 methodology, it would be just shy of 10% (that’s per year!).

Worth noting, the CPI level for gasoline in January showed a 3% decline. It will be interesting to see the impact higher prices have had over February when new figures come out next month. We doubt it will have much effect, though, since gas only accounts for about 5% of the entire CPI pie.

Getting more into the oil story, pump prices have risen roughly 50 cents over the past month alone, the biggest gain in over two years. While the price for crude oil has been rising recently similar to stocks (which shows that stimulus also helps to send commodity prices higher, not just stocks), it sold off strongly this week.

Even though prices fell this week, pump prices may stay higher in the near-term due to refinery issues (the crude oil is sold to refineries to be made into gas). Many refiners use this typically slower time of the year to conduct maintenance while also converting to the higher priced summer blends.

Additionally, a more important point to consider is that many refinery closings have taken a large amount of volume off the market, which has kept these prices higher than normal.

Next Week

Next week looks to be a busier one. The sequester appears to be one of the major stories since the cuts are scheduled to take place on Friday. As it stands now, it looks like the cuts will occur. Unfortunately, we will probably be subjected to doom and gloom, sky-is-falling threats if spending cuts were to go through. The rhetoric is embarrassingly untruthful as the cuts are insignificant (though are more significant to the military while ignoring our real spending problem, entitlements).

As for other events of the week, Fed chief Ben Bernanke will discuss the economy in his semi-annual address to the Senate. Plus there will be the much watch revision to fourth quarter GDP, which came in negative on its first posting. We will also get info on housing, consumer confidence, durable goods, personal income and spending, and manufacturing.

Lastly, an election in Italy over the weekend may turn the spotlight back on the European region.

Investment Strategy

We saw a more jittery market this week, even though it ended the week with little change. With that little change, the market still looks expensive at this level and the odds of a pullback are still high.

We continue to think increasing cash by getting out of riskier assets or buying puts (which allow us to be protected from downward moves while still participating in the upside) looks to be a good option at this time.

As for the negatives we see, economies around the world are either growing slightly or contracting, corporate earnings barely beat inflation, gas prices are high, and fights in Washington are picking up. Plus corporate insiders have sold stock at the fastest pace in two years. And somehow stocks are still at or near record highs.

The one positive we see is the Fed and other central banks around the world. We believe the money printing by the Fed has been the biggest driver of the stock rally thus far. And since the beginning of the year, they have been printing even more. While it has been of little help to the economy and will have negative long term consequences, it does send stocks higher in the meantime.

At these high levels, though, we are extremely cautious on how much higher the market can go from here.

While we aren’t looking to do any buying in the broader stock indexes at this point, we are always looking for opportunities. In individual stocks, we still like higher-quality and dividend paying ones. Companies with operations overseas have seen better earnings than those who don’t. We also like smaller and mid sized stocks that don’t have a strong correlation to the broader market and Europe.

Gold has sold-off strongly recently, but we still like it for the long term. Central banks continue to print money to stimulate their economies and weaken the currencies, a condition that favors gold. It is approaching a price level that may be a good buying opportunity.

We like other commodities for the long term, especially due to weaker currencies around the globe. A slowdown in global growth may weigh on commodity prices in the short run, though.

As for bonds, Treasury bond yields continue to move higher (so prices have fallen). A short position (bet on a decline in price) has done well here. However, we worry that this is unlikely to continue in the near-term, making the short position only a nice hedge. The potential for longer term profit is low at this time.

We also think TIPs are important as we still expect inflation to increase. Municipal bonds provide a nice way to reduce taxes, though new itemization laws may reduce their benefits in some cases.

Finally, in international stocks, we are less enthusiastic on developed markets, but not totally sold on emerging, either.

Please note, these day-to-day and week-to-week fluctuations have little impact on positions we intend to hold for several years or longer. Our short and medium term investments are the only positions affected by these daily and weekly fluctuations.

This commentary is for informational purposes and is not investment advice, an indicator of future performance, a solicitation, an offer to buy or sell, or a recommendation for any security. It should not be used as a primary basis for making investment decisions. Consider your own financial circumstances and goals carefully before investing. Past performance cannot guarantee results.

Like Icarus flying too close to the sun, the markets plunged Wednesday and Thursday for the biggest two-day drop of the year. The VIX had its worst two-day stretch in 14 months (signaling volatility and fear increasing).

To this point in the rally, much of the negative news has been overlooked. After the run it has had, though, some investors (like us) have been getting jittery and looking for an excuse to take some money off the table. Some bad news this week provided that opportunity.

On Wednesday, the Fed released the minutes of its most recent meeting in January. There appeared to be a growing concern with some Fed members that the stimulus program is causing new risks in the economy. The cheap money could cause “economic and financial imbalances” according to one Fed member. This raised the idea that the asset purchases (money printing) could be scaled back from its $85 billion a month.

The idea that the Fed may not be as committed to its stimulus program sparked the strong sell-off in the market (while reaffirming that the market gains have been fueled by the Feds actions). Other negative economic data showing a drop in manufacturing in the Philadelphia region and a gain in weekly jobless claims added to the downward pressure.

By Friday, the market reversed course for a strong gain. Part of the reason for the rise may have been an appearance by one Fed member, James Bullard, on a CNBC morning program.

He stated that the Fed will stay “very aggressive…for a very long time.” That means the markets were wrong to be worried about the Fed earlier in the week and stimulus will continue, well, for a very long time. He also noted that the program in place since the beginning of the new year was more potent, since it is outright printing of $85 billion a month (once a phenomenally large number that barely elicits a response these days).

The market moved higher on the prospect of more money printing for a very long time (and again reaffirms that the market gains are fueled by the Feds actions).

One concern of these Fed programs has been inflation. Inflation reports released this week, the CPI and PPI, showed little to no gain in inflation over the month of January. The level remains well below the inflation target the Fed would like to see.

As anyone in the real world can attest to (as well as professionals who dig into the nuances of its calculation), the inflation results are laughable. According to shadowstats.com, if inflation today were to be measured using 1990 methodology, inflation would be running closer to 5%. Under 1980 methodology, it would be just shy of 10% (that’s per year!).

Worth noting, the CPI level for gasoline in January showed a 3% decline. It will be interesting to see the impact higher prices have had over February when new figures come out next month. We doubt it will have much effect, though, since gas only accounts for about 5% of the entire CPI pie.

Getting more into the oil story, pump prices have risen roughly 50 cents over the past month alone, the biggest gain in over two years. While the price for crude oil has been rising recently similar to stocks (which shows that stimulus also helps to send commodity prices higher, not just stocks), it sold off strongly this week.

Even though prices fell this week, pump prices may stay higher in the near-term due to refinery issues (the crude oil is sold to refineries to be made into gas). Many refiners use this typically slower time of the year to conduct maintenance while also converting to the higher priced summer blends.

Additionally, a more important point to consider is that many refinery closings have taken a large amount of volume off the market, which has kept these prices higher than normal.

Next Week

Next week looks to be a busier one. The sequester appears to be one of the major stories since the cuts are scheduled to take place on Friday. As it stands now, it looks like the cuts will occur. Unfortunately, we will probably be subjected to doom and gloom, sky-is-falling threats if spending cuts were to go through. The rhetoric is embarrassingly untruthful as the cuts are insignificant (though are more significant to the military while ignoring our real spending problem, entitlements).

As for other events of the week, Fed chief Ben Bernanke will discuss the economy in his semi-annual address to the Senate. Plus there will be the much watch revision to fourth quarter GDP, which came in negative on its first posting. We will also get info on housing, consumer confidence, durable goods, personal income and spending, and manufacturing.

Lastly, an election in Italy over the weekend may turn the spotlight back on the European region.

Investment Strategy

We saw a more jittery market this week, even though it ended the week with little change. With that little change, the market still looks expensive at this level and the odds of a pullback are still high.

We continue to think increasing cash by getting out of riskier assets or buying puts (which allow us to be protected from downward moves while still participating in the upside) looks to be a good option at this time.

As for the negatives we see, economies around the world are either growing slightly or contracting, corporate earnings barely beat inflation, gas prices are high, and fights in Washington are picking up. Plus corporate insiders have sold stock at the fastest pace in two years. And somehow stocks are still at or near record highs.

The one positive we see is the Fed and other central banks around the world. We believe the money printing by the Fed has been the biggest driver of the stock rally thus far. And since the beginning of the year, they have been printing even more. While it has been of little help to the economy and will have negative long term consequences, it does send stocks higher in the meantime.

At these high levels, though, we are extremely cautious on how much higher the market can go from here.

While we aren’t looking to do any buying in the broader stock indexes at this point, we are always looking for opportunities. In individual stocks, we still like higher-quality and dividend paying ones. Companies with operations overseas have seen better earnings than those who don’t. We also like smaller and mid sized stocks that don’t have a strong correlation to the broader market and Europe.

Gold has sold-off strongly recently, but we still like it for the long term. Central banks continue to print money to stimulate their economies and weaken the currencies, a condition that favors gold. It is approaching a price level that may be a good buying opportunity.

We like other commodities for the long term, especially due to weaker currencies around the globe. A slowdown in global growth may weigh on commodity prices in the short run, though.

As for bonds, Treasury bond yields continue to move higher (so prices have fallen). A short position (bet on a decline in price) has done well here. However, we worry that this is unlikely to continue in the near-term, making the short position only a nice hedge. The potential for longer term profit is low at this time.

We also think TIPs are important as we still expect inflation to increase. Municipal bonds provide a nice way to reduce taxes, though new itemization laws may reduce their benefits in some cases.

Finally, in international stocks, we are less enthusiastic on developed markets, but not totally sold on emerging, either.

Please note, these day-to-day and week-to-week fluctuations have little impact on positions we intend to hold for several years or longer. Our short and medium term investments are the only positions affected by these daily and weekly fluctuations.

This commentary is for informational purposes and is not investment advice, an indicator of future performance, a solicitation, an offer to buy or sell, or a recommendation for any security. It should not be used as a primary basis for making investment decisions. Consider your own financial circumstances and goals carefully before investing. Past performance cannot guarantee results.