We had a bit of a roller coaster ride this week as the markets continued to move lower, notching the worst returns of the year. For the week, the Dow was lower by 1.6%, the S&P fell 2.0%, and the Nasdaq returned -2.3%. Gold rose from its recent lows, climbing 1.9% to $1,659 an ounce. Oil has also shown weakness recently and sold off slightly this week, down 0.5% to $102.83 per barrel. Brent crude closed slightly over $121 per barrel.

Source: MSN Moneycentral

Source: MSN Moneycentral

The markets opened the week with a steep drop, largely due to the disappointing employment report that was released the prior Friday. The drop continued the trend that started in the prior week, when the latest Fed minutes were interpreted that Chairman Bernanke was unlikely to do another stimulus.

Adding to the downward pressure on stocks, worries in Europe are again rising as investors focus on the economic and debt problems in Spain and Italy. Their ability to reduce that debt has come into question, as well. Dramatic spending cuts have been implemented and are badly needed.

Taxes have been increased in an attempt to raise revenue, but that revenue rarely materializes with tax hikes. A growing economy is the way to increase tax revenues, and higher taxes choke off the necessary growth. In our opinion, a lower tax rate would be favorable to the burdensome high rates many European countries have implemented. Ultimately, we believe the solutions in place will fail.

Slowing growth in China also weighed on the market this week. Though the economy grew at an 8.1% rate in the latest quarter, it is the lowest level of growth since early 2009. Plus, there is a general level of distrust with their government-released data, so there is a concern that the real growth rate is much lower than this.

As we mentioned above, the catalyst for the recent downturn was the speculation of no further stimulus (or quantitative easing, or QE) from the Fed. This week continued the guessing game on the likelihood of future stimulus.

Two Fed officials made headlines with their discussions of new stimulus. The Vice Chairman of the Fed and number two in charge, Janet Yellen, indicated that weaknesses persist in the economy and additional stimulus may be warranted. The Fed has announced that they will hold interest rates at these historically low levels until 2014, but Vice Chair Yellen noted it may be even longer. In a separate speech, the President of the NY Fed made similar remarks.

Since the actions of the Fed have been the primary driver of the stock market, the prospect of new stimulus helped send markets higher.

Corporate earnings for the first quarter began coming in this week. Expectations have been ratcheted lower, so the bar is not set very high here. The average estimate for earnings growth this quarter is just under 1%. Keep in mind, last quarter saw an 8% growth, while the quarter before that had 18% growth.

The earnings released this week were not bad. At least, not at first glance. For some of the bigger names, aluminum producer Alcoa saw a growth in revenue, but had higher costs that lowered overall earnings.

Google saw a nice increase in revenue and even announced a dividend and a stock split (likely to keep up with Apple). However, that splitting of the shares would result in even more power being consolidated to the firm’s founders, and that didn’t go over well with investors. The stock sold off sharply.

Two banks were the other big releases, with both Wells Fargo and JP Morgan turning in nice results. However, higher costs and poor loan growth caught investor’s attention and those stocks sold off, as well.

Continuing that negative theme, economic data this week was rather poor. Weekly unemployment data showed a sharp rise. Small business and consumer sentiment was also lackluster.

Inflation remains above the Fed’s target of 2% with the CPI rising 0.3% last month for a 2.7% annualized number. It’s funny, because the Fed is constantly mentioning how inflation is running below target, but it has been persistently above their stated target of 2%. Inflation is not a concern in their eyes, but is a significant burden when buying groceries or filling up the gas tank.

Next Week

Economic data next week will be relatively light, but corporate earnings will begin coming in at a steady pace. We will get info on retail sales, industrial production, leading economic indicators, and some data on housing.

For corporate earnings, we will get releases from some bigger names like Citigroup, Coca-Cola, IBM, GE, Yum Brands, and McDonald’s.

Investment Strategy

We were not surprised by the recent sell-off and used the opportunity to add to positions mid-week. The market appears oversold in the short term, but we have concerns for the longer term.

We worry that as the latest round of stimulus wears off in June, the market will drop, just like it did at the conclusion of the previous two stimuli.

We worry that as the latest round of stimulus wears off in June, the market will drop, just like it did at the conclusion of the previous two stimuli.

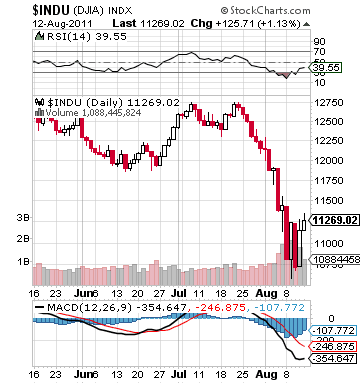

The chart on the right shows what happened last summer when the stimulus ended. The recent activity of the market is reminiscent of last June, where the market fell and rose again. Unfortunately the market plunged a month later, and that is our concern.

On pull-backs, we look to add to positions in large cap higher-quality and dividend paying stocks, particularly companies with operations overseas. Smaller and little-known stocks with low correlation to the market are also promising. Also, there is always the opportunity to find undervalued individual stocks at any point.

We like commodities for the long term but fear a slowdown in China and the other BRIC countries (Brazil, Russia, and India), who have been major drivers of commodity prices. Debt problems and continuing bailouts around the world should be favorable to commodities like gold in the long term. We are still hesitant to add more at current prices.

A short Treasury Bond position (bet on a decline in value) provides a nice hedge here, but we think the potential for profit is low at the moment.

On the bond theme, we think TIPs are important as we still expect inflation to increase. Municipal bonds also work and there are some nice yielding bonds out there now (try to avoid muni funds and buy the actual bond if possible).

Finally, in international stocks, we favor developed international markets as opposed to emerging.

These day-to-day and week-to-week fluctuations have little impact on positions we intend to hold for several years or longer. Our short and medium term investments are the only positions affected by these daily and weekly fluctuations.

This commentary is for informational purposes and is not investment advice, an indicator of future performance, a solicitation, an offer to buy or sell, or a recommendation for any security. It should not be used as a primary basis for making investment decisions. Consider your own financial circumstances and goals carefully before investing. Past performance cannot guarantee results.

Source: MSN Moneycentral

Source: MSN MoneycentralThe markets opened the week with a steep drop, largely due to the disappointing employment report that was released the prior Friday. The drop continued the trend that started in the prior week, when the latest Fed minutes were interpreted that Chairman Bernanke was unlikely to do another stimulus.

Adding to the downward pressure on stocks, worries in Europe are again rising as investors focus on the economic and debt problems in Spain and Italy. Their ability to reduce that debt has come into question, as well. Dramatic spending cuts have been implemented and are badly needed.

Taxes have been increased in an attempt to raise revenue, but that revenue rarely materializes with tax hikes. A growing economy is the way to increase tax revenues, and higher taxes choke off the necessary growth. In our opinion, a lower tax rate would be favorable to the burdensome high rates many European countries have implemented. Ultimately, we believe the solutions in place will fail.

Slowing growth in China also weighed on the market this week. Though the economy grew at an 8.1% rate in the latest quarter, it is the lowest level of growth since early 2009. Plus, there is a general level of distrust with their government-released data, so there is a concern that the real growth rate is much lower than this.

As we mentioned above, the catalyst for the recent downturn was the speculation of no further stimulus (or quantitative easing, or QE) from the Fed. This week continued the guessing game on the likelihood of future stimulus.

Two Fed officials made headlines with their discussions of new stimulus. The Vice Chairman of the Fed and number two in charge, Janet Yellen, indicated that weaknesses persist in the economy and additional stimulus may be warranted. The Fed has announced that they will hold interest rates at these historically low levels until 2014, but Vice Chair Yellen noted it may be even longer. In a separate speech, the President of the NY Fed made similar remarks.

Since the actions of the Fed have been the primary driver of the stock market, the prospect of new stimulus helped send markets higher.

Corporate earnings for the first quarter began coming in this week. Expectations have been ratcheted lower, so the bar is not set very high here. The average estimate for earnings growth this quarter is just under 1%. Keep in mind, last quarter saw an 8% growth, while the quarter before that had 18% growth.

The earnings released this week were not bad. At least, not at first glance. For some of the bigger names, aluminum producer Alcoa saw a growth in revenue, but had higher costs that lowered overall earnings.

Google saw a nice increase in revenue and even announced a dividend and a stock split (likely to keep up with Apple). However, that splitting of the shares would result in even more power being consolidated to the firm’s founders, and that didn’t go over well with investors. The stock sold off sharply.

Two banks were the other big releases, with both Wells Fargo and JP Morgan turning in nice results. However, higher costs and poor loan growth caught investor’s attention and those stocks sold off, as well.

Continuing that negative theme, economic data this week was rather poor. Weekly unemployment data showed a sharp rise. Small business and consumer sentiment was also lackluster.

Inflation remains above the Fed’s target of 2% with the CPI rising 0.3% last month for a 2.7% annualized number. It’s funny, because the Fed is constantly mentioning how inflation is running below target, but it has been persistently above their stated target of 2%. Inflation is not a concern in their eyes, but is a significant burden when buying groceries or filling up the gas tank.

Next Week

Economic data next week will be relatively light, but corporate earnings will begin coming in at a steady pace. We will get info on retail sales, industrial production, leading economic indicators, and some data on housing.

For corporate earnings, we will get releases from some bigger names like Citigroup, Coca-Cola, IBM, GE, Yum Brands, and McDonald’s.

Investment Strategy

We were not surprised by the recent sell-off and used the opportunity to add to positions mid-week. The market appears oversold in the short term, but we have concerns for the longer term.

We worry that as the latest round of stimulus wears off in June, the market will drop, just like it did at the conclusion of the previous two stimuli.

We worry that as the latest round of stimulus wears off in June, the market will drop, just like it did at the conclusion of the previous two stimuli. The chart on the right shows what happened last summer when the stimulus ended. The recent activity of the market is reminiscent of last June, where the market fell and rose again. Unfortunately the market plunged a month later, and that is our concern.

On pull-backs, we look to add to positions in large cap higher-quality and dividend paying stocks, particularly companies with operations overseas. Smaller and little-known stocks with low correlation to the market are also promising. Also, there is always the opportunity to find undervalued individual stocks at any point.

We like commodities for the long term but fear a slowdown in China and the other BRIC countries (Brazil, Russia, and India), who have been major drivers of commodity prices. Debt problems and continuing bailouts around the world should be favorable to commodities like gold in the long term. We are still hesitant to add more at current prices.

A short Treasury Bond position (bet on a decline in value) provides a nice hedge here, but we think the potential for profit is low at the moment.

On the bond theme, we think TIPs are important as we still expect inflation to increase. Municipal bonds also work and there are some nice yielding bonds out there now (try to avoid muni funds and buy the actual bond if possible).

Finally, in international stocks, we favor developed international markets as opposed to emerging.

These day-to-day and week-to-week fluctuations have little impact on positions we intend to hold for several years or longer. Our short and medium term investments are the only positions affected by these daily and weekly fluctuations.

This commentary is for informational purposes and is not investment advice, an indicator of future performance, a solicitation, an offer to buy or sell, or a recommendation for any security. It should not be used as a primary basis for making investment decisions. Consider your own financial circumstances and goals carefully before investing. Past performance cannot guarantee results.