Stocks turned in their first weekly decline since early October. Through the close Friday, the Dow was lower by 0.4%, the S&P fell a miniscule 0.04%, while the Nasdaq eked out a gain of 0.06%. Bond yields hit their highest level since September, so their prices have fallen. Gold saw a lot of activity, only to close with a loss of 1.6%. Oil rose fairly sharply, climbing 5.3% to $97.65 per barrel. The other major type of oil, Brent, saw far less movement to close at $111.25 per barrel.

Source: Yahoo Finance

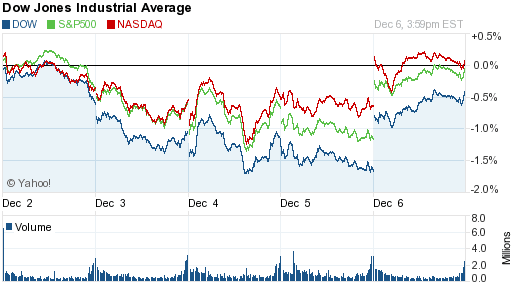

Economic data played a large part in the movement of the market this week. However, the reaction in stocks was the opposite of what you might think. Positive reports sent stocks lower and negative or mediocre reports sent stocks higher.

Unfortunately this requires talking about the Fed again. Economic reports are being scrutinized for their impact on the Fed’s stimulus program. Positive economic reports mean less need for stimulus, so they increase the chances that the Fed will pull back on these programs. Since the money printed by the Fed has fueled the rise in stocks, positive reports send stocks lower.

As can be seen in the chart above, positive reports were the story for the majority of the week. Touching on some of these reports, the manufacturing sector showed a solid gain over the last month. The service sector expanded, as well, though not as much as many hoped.

Also, the Fed’s Beige Book, which surveys economic conditions over the Fed districts showed continued “modest to moderate” growth (worth noting, businesses are still concerned about costs from the new healthcare law). Third quarter GDP was revised higher to a solid 3.6% growth, though it should be noted the bulk of the gains came from businesses increasing inventories, not necessarily from rising sales.

Employment saw several important reports this week, too. Reports released early in the week showed a fairly solid improvement in the employment situation.

This brings us to Friday. Stocks rose sharply when the important government employment report showed a solid increase of 203,000 jobs in November. Additionally, the unemployment rate fell from 7.3% to 7.0%, its lowest level in five years, although this was more due to the nuances in how the rate is calculated (the number of employed improved, but the labor force increased by a larger amount). When comparing the amount of people working to the total population of the country, this metric has not seen the same improvement, holding flat since late 2009 (LINK).

With positive reports sending stocks lower all week, why did this seemingly good report send stocks higher? While it may have been good, it looks like it wasn’t good enough to trigger an immediate reduction in stimulus at the Fed’s next meeting in two weeks. At least, that’s the best explanation we’ve seen for the reaction in the market.

Finally, retail sales were another important story this week. It appears that spending over the Thanksgiving shopping period was lower than a year ago. Actually, there were more people out shopping and bought more items, but they spent less overall. This is not a good indicator for the economy. It means people are worried about their financial situation, where they seek out sales to afford their gifts.

Next Week

Next week looks to be pretty quiet for economic data. We’ll get information on retail sales, import prices, and inflation at the producer level. All eyes will be on the Fed, though, as they hold another meeting the following week. Investors are watching closely for clues on a tapering in the stimulus program, so be prepared for another week focused on the Fed.

Investment Strategy

Stocks came off their highs and look a little less expensive here in the shorter run. Many investors are worried that the Fed will announce a reduction in their stimulus program at their December 18th meeting, which has pressured stocks lower. We think that is still highly unlikely and stocks have the potential to rise strongly if that is the case. Regardless, we wouldn’t put new money into the broader market at this time as stocks are still on the expensive side.

We still have worries for the longer run. This includes concerns over the unintended consequences from the Fed creating massive amounts of money out of thin air, slowing earnings growth, still-high valuation ratios, record high margin (borrowing to buy stocks) levels, massive amounts of new money coming into stock funds, and exuberance around the IPO market.

While we wouldn’t add any new money to stock market indexes at this point, we prefer finding undervalued individual names to invest in. Fundamental analysis tells us how good a company is, while the technical (or the charts) side gives us a good idea of when to buy. We would avoid stocks in sectors with a strong correlation to the broader stock market and interest rates. Our timeframe is shorter (looking out a couple weeks or months), so we can keep one foot out the door in case the market turns abruptly.

Bonds have been volatile recently as yields are again rising (so prices are falling). A short position (bet on the decline in prices) has done well here, but serves only as a nice hedge. It isn’t intended to be a longer term investment.

TIPs have shown weakness recently, however, they remain an important hedge against future inflation. Municipal bonds are in the same boat and work for the right client. We like buying individual, insured names for these bonds, avoiding muni index bonds if possible. We keep a longer term focus with these investments.

Gold continues to look weak, continuing the volatility this investment has seen recently. It’s good as a long term hedge, but caution is warranted.

We like other commodities for the long term, especially due to weaker currencies around the globe. A slowdown in global growth seems to be weighing on commodity prices here, so buying on the dips may work with a longer time horizon.

Finally, in international stocks, we are still not interested in developed markets and not totally sold on emerging, either.

Please note, these day-to-day and week-to-week fluctuations have little impact on positions we intend to hold for several years or longer. Our short and medium term investments are the only positions affected by these daily and weekly fluctuations.

This commentary is for informational purposes and is not investment advice, an indicator of future performance, a solicitation, an offer to buy or sell, or a recommendation for any security. It should not be used as a primary basis for making investment decisions. Consider your own financial circumstances and goals carefully before investing. Past performance cannot guarantee results.

Unfortunately this requires talking about the Fed again. Economic reports are being scrutinized for their impact on the Fed’s stimulus program. Positive economic reports mean less need for stimulus, so they increase the chances that the Fed will pull back on these programs. Since the money printed by the Fed has fueled the rise in stocks, positive reports send stocks lower.

As can be seen in the chart above, positive reports were the story for the majority of the week. Touching on some of these reports, the manufacturing sector showed a solid gain over the last month. The service sector expanded, as well, though not as much as many hoped.

Also, the Fed’s Beige Book, which surveys economic conditions over the Fed districts showed continued “modest to moderate” growth (worth noting, businesses are still concerned about costs from the new healthcare law). Third quarter GDP was revised higher to a solid 3.6% growth, though it should be noted the bulk of the gains came from businesses increasing inventories, not necessarily from rising sales.

Employment saw several important reports this week, too. Reports released early in the week showed a fairly solid improvement in the employment situation.

This brings us to Friday. Stocks rose sharply when the important government employment report showed a solid increase of 203,000 jobs in November. Additionally, the unemployment rate fell from 7.3% to 7.0%, its lowest level in five years, although this was more due to the nuances in how the rate is calculated (the number of employed improved, but the labor force increased by a larger amount). When comparing the amount of people working to the total population of the country, this metric has not seen the same improvement, holding flat since late 2009 (LINK).

With positive reports sending stocks lower all week, why did this seemingly good report send stocks higher? While it may have been good, it looks like it wasn’t good enough to trigger an immediate reduction in stimulus at the Fed’s next meeting in two weeks. At least, that’s the best explanation we’ve seen for the reaction in the market.

Finally, retail sales were another important story this week. It appears that spending over the Thanksgiving shopping period was lower than a year ago. Actually, there were more people out shopping and bought more items, but they spent less overall. This is not a good indicator for the economy. It means people are worried about their financial situation, where they seek out sales to afford their gifts.

Next Week

Next week looks to be pretty quiet for economic data. We’ll get information on retail sales, import prices, and inflation at the producer level. All eyes will be on the Fed, though, as they hold another meeting the following week. Investors are watching closely for clues on a tapering in the stimulus program, so be prepared for another week focused on the Fed.

Investment Strategy

Stocks came off their highs and look a little less expensive here in the shorter run. Many investors are worried that the Fed will announce a reduction in their stimulus program at their December 18th meeting, which has pressured stocks lower. We think that is still highly unlikely and stocks have the potential to rise strongly if that is the case. Regardless, we wouldn’t put new money into the broader market at this time as stocks are still on the expensive side.

We still have worries for the longer run. This includes concerns over the unintended consequences from the Fed creating massive amounts of money out of thin air, slowing earnings growth, still-high valuation ratios, record high margin (borrowing to buy stocks) levels, massive amounts of new money coming into stock funds, and exuberance around the IPO market.

While we wouldn’t add any new money to stock market indexes at this point, we prefer finding undervalued individual names to invest in. Fundamental analysis tells us how good a company is, while the technical (or the charts) side gives us a good idea of when to buy. We would avoid stocks in sectors with a strong correlation to the broader stock market and interest rates. Our timeframe is shorter (looking out a couple weeks or months), so we can keep one foot out the door in case the market turns abruptly.

Bonds have been volatile recently as yields are again rising (so prices are falling). A short position (bet on the decline in prices) has done well here, but serves only as a nice hedge. It isn’t intended to be a longer term investment.

TIPs have shown weakness recently, however, they remain an important hedge against future inflation. Municipal bonds are in the same boat and work for the right client. We like buying individual, insured names for these bonds, avoiding muni index bonds if possible. We keep a longer term focus with these investments.

Gold continues to look weak, continuing the volatility this investment has seen recently. It’s good as a long term hedge, but caution is warranted.

We like other commodities for the long term, especially due to weaker currencies around the globe. A slowdown in global growth seems to be weighing on commodity prices here, so buying on the dips may work with a longer time horizon.

Finally, in international stocks, we are still not interested in developed markets and not totally sold on emerging, either.

Please note, these day-to-day and week-to-week fluctuations have little impact on positions we intend to hold for several years or longer. Our short and medium term investments are the only positions affected by these daily and weekly fluctuations.

This commentary is for informational purposes and is not investment advice, an indicator of future performance, a solicitation, an offer to buy or sell, or a recommendation for any security. It should not be used as a primary basis for making investment decisions. Consider your own financial circumstances and goals carefully before investing. Past performance cannot guarantee results.