Please note: there will be no market commentary next week due to the 4th of July holiday. We hope you have a great weekend.

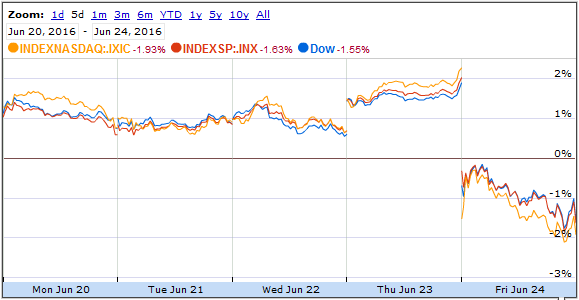

A sizeable loss Friday put stocks into negative territory for the week. Through Friday’s close, the Dow and S&P 500 both lost 1.6% and the Nasdaq was down 1.9%. U.S. bond yields rose off four-year lows this week (so prices fell), but strongly reversed course Friday to again close near four year lows. Gold hit its highest level in two years with a 1.54% rise. Oil fell 1.4% close at $47.57. The international Brent oil declined to 49.04.

A sizeable loss Friday put stocks into negative territory for the week. Through Friday’s close, the Dow and S&P 500 both lost 1.6% and the Nasdaq was down 1.9%. U.S. bond yields rose off four-year lows this week (so prices fell), but strongly reversed course Friday to again close near four year lows. Gold hit its highest level in two years with a 1.54% rise. Oil fell 1.4% close at $47.57. The international Brent oil declined to 49.04.

Source: Google Finance

By now you’ve probably heard about the “Brexit” vote, where Britain voted to leave the European Union. The result sent markets into a panic and only safe-haven assets like gold or the dollar made it out unscathed. Stocks had their worst day since August 2015.

The polls leading up to the vote increasingly showed a “remain” outcome was likely, though it was still a close race. A “leave” vote would bring uncertainty to the markets – and the market hates uncertainty – so the polls showing “remain” reassured the markets and they rose steadily through Thursday.

Of course, the vote did not go the way mot expected. The markets face a new uncertainty since no one knows how the unwinding of Britain from the E.U. will play out. The exit won’t happen overnight, though, as they have a couple years to work it out.

There are also concerns of an entire unraveling of the E.U. experiment. There are many unhappy countries in the E.U. Now knowing it is possible to leave, they may looking into doing so, or at least trying to renegotiate better terms to prevent them from leaving. This can cause a domino effect that no one knows how will play out.

We think this will be a positive in the long run for both England and Europe, but it could get pretty messy in the meantime.

Getting to the other news of the week, Fed chief Janet Yellen made her semi-annual testimony in front of Congress this week. It was mostly a non-event as she told us little we didn’t expect.

However, the tone was quite a remarkable change from just a few weeks ago. At that time, we were talking about how an interest rate increase looked likely. A few poor economic reports in the meantime and there isn’t a hint of an increase in interest rates in the coming months. In fact, the odds show a greater chance of lower interest rates in the coming months rather than higher ones.

Finally, economic data this week leaned to the negative side. Existing home sales are at their strongest pace since 2007, but the pace of new home sales fell sharply. Also, durable goods fell much more than expected last month.

Next Week

The focus next week is likely to still be on the effects of the British vote. It could be another volatile week for the markets.

We will get a couple economic reports worth watching, including the revision to first quarter GDP and the strength of the manufacturing sector. We’ll also get info on housing and personal income and spending.

Central bank leaders from around the world, including our Fed, are also holding a meeting in Europe next week and we’re sure investors will be closely watching what they have to say.

Investment Strategy

The question now is, did Friday’s decline provide a good buying opportunity? Of course, no one knows for sure and it’s likely the next few weeks will be more volatile than average.

However, next week marks the end of the quarter and you often see buying at that time as investors try to squeeze out some extra returns to help their performance metrics. That might help support stocks for the next several days.

Either way, we are bracing for a more volatile, active market in the coming weeks.

We can say we are very cautious in the longer-term. The stimulus of the last several years masked many problems, causing a misallocation of resources and allowing bubbles to form. It also prevented necessary changes from occurring at both a corporate and political level. If the stimulus is ever forced to end, those flaws become more apparent. We’re now seeing lower corporate earnings, massive debt levels, poor economic growth, and potential for recession. This will weigh on the market at some point, but the question remains as to when.

Bonds saw a lot of activity this week. We think prices will remain high and yields low. They are at extraordinary levels now so the trend may reverse, but we don’t think by much. Our relatively higher-yielding bonds are seen as more attractive to other bonds around the world. We think this dynamic and a “flight to safety” will keep prices high for a considerable time.

Bonds to protect against inflation, or TIPs, remain a good long term hedge for inflation. Floating-rate bonds will do well if interest rates eventually do rise.

Some municipal bonds look attractive for the right client, too. We like buying individual, insured names for these bonds, avoiding muni index bonds if possible. We keep a longer term focus with these investments.

Gold is another good hedge for the portfolio. It is only a hedge at this point – rising on geopolitical issues and a flight to safety.

Finally, in international stocks, we see weakness around the globe and favor neither the developed or emerging markets.

Please note, these day-to-day and week-to-week fluctuations have little impact on positions we intend to hold for several years or longer. Our short and medium term investments are the only positions affected by these daily and weekly fluctuations.

This commentary is for informational purposes and is not investment advice, an indicator of future performance, a solicitation, an offer to buy or sell, or a recommendation for any security. It should not be used as a primary basis for making investment decisions. Consider your own financial circumstances and goals carefully before investing. Past performance cannot guarantee results.

The polls leading up to the vote increasingly showed a “remain” outcome was likely, though it was still a close race. A “leave” vote would bring uncertainty to the markets – and the market hates uncertainty – so the polls showing “remain” reassured the markets and they rose steadily through Thursday.

Of course, the vote did not go the way mot expected. The markets face a new uncertainty since no one knows how the unwinding of Britain from the E.U. will play out. The exit won’t happen overnight, though, as they have a couple years to work it out.

There are also concerns of an entire unraveling of the E.U. experiment. There are many unhappy countries in the E.U. Now knowing it is possible to leave, they may looking into doing so, or at least trying to renegotiate better terms to prevent them from leaving. This can cause a domino effect that no one knows how will play out.

We think this will be a positive in the long run for both England and Europe, but it could get pretty messy in the meantime.

Getting to the other news of the week, Fed chief Janet Yellen made her semi-annual testimony in front of Congress this week. It was mostly a non-event as she told us little we didn’t expect.

However, the tone was quite a remarkable change from just a few weeks ago. At that time, we were talking about how an interest rate increase looked likely. A few poor economic reports in the meantime and there isn’t a hint of an increase in interest rates in the coming months. In fact, the odds show a greater chance of lower interest rates in the coming months rather than higher ones.

Finally, economic data this week leaned to the negative side. Existing home sales are at their strongest pace since 2007, but the pace of new home sales fell sharply. Also, durable goods fell much more than expected last month.

Next Week

The focus next week is likely to still be on the effects of the British vote. It could be another volatile week for the markets.

We will get a couple economic reports worth watching, including the revision to first quarter GDP and the strength of the manufacturing sector. We’ll also get info on housing and personal income and spending.

Central bank leaders from around the world, including our Fed, are also holding a meeting in Europe next week and we’re sure investors will be closely watching what they have to say.

Investment Strategy

The question now is, did Friday’s decline provide a good buying opportunity? Of course, no one knows for sure and it’s likely the next few weeks will be more volatile than average.

However, next week marks the end of the quarter and you often see buying at that time as investors try to squeeze out some extra returns to help their performance metrics. That might help support stocks for the next several days.

Either way, we are bracing for a more volatile, active market in the coming weeks.

We can say we are very cautious in the longer-term. The stimulus of the last several years masked many problems, causing a misallocation of resources and allowing bubbles to form. It also prevented necessary changes from occurring at both a corporate and political level. If the stimulus is ever forced to end, those flaws become more apparent. We’re now seeing lower corporate earnings, massive debt levels, poor economic growth, and potential for recession. This will weigh on the market at some point, but the question remains as to when.

Bonds saw a lot of activity this week. We think prices will remain high and yields low. They are at extraordinary levels now so the trend may reverse, but we don’t think by much. Our relatively higher-yielding bonds are seen as more attractive to other bonds around the world. We think this dynamic and a “flight to safety” will keep prices high for a considerable time.

Bonds to protect against inflation, or TIPs, remain a good long term hedge for inflation. Floating-rate bonds will do well if interest rates eventually do rise.

Some municipal bonds look attractive for the right client, too. We like buying individual, insured names for these bonds, avoiding muni index bonds if possible. We keep a longer term focus with these investments.

Gold is another good hedge for the portfolio. It is only a hedge at this point – rising on geopolitical issues and a flight to safety.

Finally, in international stocks, we see weakness around the globe and favor neither the developed or emerging markets.

Please note, these day-to-day and week-to-week fluctuations have little impact on positions we intend to hold for several years or longer. Our short and medium term investments are the only positions affected by these daily and weekly fluctuations.

This commentary is for informational purposes and is not investment advice, an indicator of future performance, a solicitation, an offer to buy or sell, or a recommendation for any security. It should not be used as a primary basis for making investment decisions. Consider your own financial circumstances and goals carefully before investing. Past performance cannot guarantee results.