It was another rough week for the market. Through the close Friday, the Dow was lower by 0.8%, the S&P lost 0.7%, and the Nasdaq fell 0.6%. Investors seeking safety pushed bond prices higher as yields went lower. Gold moved slightly lower on the week, off 0.3%. Oil was also lower, down 0.3% to $48.73 per barrel. The international Brent oil closed at $52.86.

Source: Google Finance

This week was an unusual one in that we had the best day for stocks since April and also had the worst day since May. It’s safe to say volatility has returned.

There were many stories driving the markets this week. Washington, the Fed, corporate earnings, and the terror attack in Barcelona all played a part.

News out of Washington consumed most of the oxygen, but it didn’t have much impact on the market as stocks were higher while the drama unfolded.

The early rise in stocks could at least partially be attributed to cooling tensions in North Korea over the weekend and the “buy-the-dippers” moving back into the market. It wasn’t until later in the week that cracks emerged.

First, there were rumors that President Trump’s chief economic advisor, Gary Cohn, would be leaving the administration. He is a very pro-growth, pro-business and his departure was a worry to the market. The rumor was incorrect and quickly refuted and the market rebounded as a result.

The reaction in the market shows how badly investors want pro-business reforms. Unfortunately those reforms seem less and less likely. Companies in a high tax bracket are a good proxy for pro-business policies since they stand to benefit the most. As you can see in the chart below, they rose immediately after the election but have been losing ground ever since.

There were many stories driving the markets this week. Washington, the Fed, corporate earnings, and the terror attack in Barcelona all played a part.

News out of Washington consumed most of the oxygen, but it didn’t have much impact on the market as stocks were higher while the drama unfolded.

The early rise in stocks could at least partially be attributed to cooling tensions in North Korea over the weekend and the “buy-the-dippers” moving back into the market. It wasn’t until later in the week that cracks emerged.

First, there were rumors that President Trump’s chief economic advisor, Gary Cohn, would be leaving the administration. He is a very pro-growth, pro-business and his departure was a worry to the market. The rumor was incorrect and quickly refuted and the market rebounded as a result.

The reaction in the market shows how badly investors want pro-business reforms. Unfortunately those reforms seem less and less likely. Companies in a high tax bracket are a good proxy for pro-business policies since they stand to benefit the most. As you can see in the chart below, they rose immediately after the election but have been losing ground ever since.

The Fed also weighed on the market this week. The minutes from their latest policy meeting were released and showed a split between members who think the Fed should continue to pull back on its stimulus policy and those who are taking more of a “wait-and-see” approach. The Fed likes to have more consensus before changing policy, so the odds of another reduction in stimulus by raising interest rates (which will make it more costly to borrow money) have fallen sharply.

Normally this would make the market happy since it means the stimulus is likely to be around longer. However, some comments in the minutes caught investors off-guard.

From the minutes: “Vulnerabilities associated with asset valuation pressures had edged up from notable to elevated.” This means worries are growing that their policies are pushing markets too high and creating bubbles. This type of language is new and signals the Fed may not be interested in pushing markets higher or supporting them should there be another correction.

Also weighing on the market was corporate earnings. Earnings have been very good so far, rising about 10% according to Factset. This has helped the markets move higher recently. However, some investors believe this is the peak of earnings and they will start moving lower in the coming quarters. Several companies warned about future earnings and investors are starting to take notice.

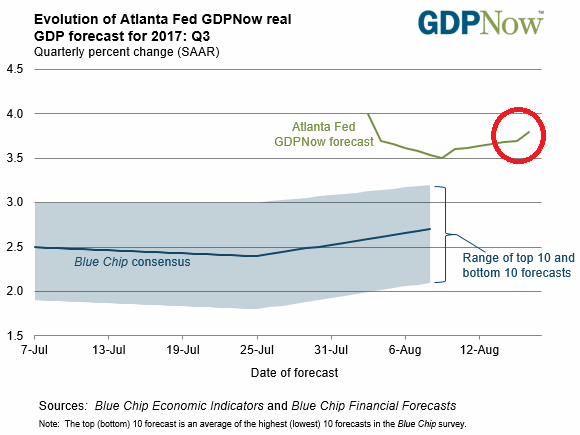

It wasn’t all bad news this week. Economic data was mostly positive. Retail sales came in at their best level since December and industrial production rose for another month.

This has caused economists to raise their GDP forecasts for the quarter. Below is the forecast from the Atlanta Fed’s “GDP Now” which has been a fairly accurate predictor of GDP. The Atlanta Fed’s prediction is the brown line while the consensus of other economists is the blue shaded region.

From the minutes: “Vulnerabilities associated with asset valuation pressures had edged up from notable to elevated.” This means worries are growing that their policies are pushing markets too high and creating bubbles. This type of language is new and signals the Fed may not be interested in pushing markets higher or supporting them should there be another correction.

Also weighing on the market was corporate earnings. Earnings have been very good so far, rising about 10% according to Factset. This has helped the markets move higher recently. However, some investors believe this is the peak of earnings and they will start moving lower in the coming quarters. Several companies warned about future earnings and investors are starting to take notice.

It wasn’t all bad news this week. Economic data was mostly positive. Retail sales came in at their best level since December and industrial production rose for another month.

This has caused economists to raise their GDP forecasts for the quarter. Below is the forecast from the Atlanta Fed’s “GDP Now” which has been a fairly accurate predictor of GDP. The Atlanta Fed’s prediction is the brown line while the consensus of other economists is the blue shaded region.

Finally, it looks like the eagles have returned to their nest outside our office. The nest had been vacant for several weeks, but it doesn’t look like the ospreys which formerly occupied the nest are ready to leave and are putting up a fight.

Next Week

Economic data will be light next week. We’ll get some info on housing and durable goods, and that’s about it.

The big news will come from the central banks. The Fed is holding their annual symposium in Jackson Hole and policy changes are often discussed at the event. Leaders of our Fed and the European Central Bank will hold discussions and investors will be watching closely.

Investment Strategy

We weren’t surprised to see stocks rebound higher early in the week after last week’s selloff. However, we were surprised when stocks sold off so strongly later in the week.

One item we’re keeping an eye on is market breadth. “Breadth,” without getting too specific, is the amount of stocks moving higher versus ones moving lower.

The chart below shows that starting in late July, more and more stocks were moving lower and the amount of bullish (or positive) stocks and the amount of stocks trading below their recent averages has also been trending lower. Yet the market remained high. This is a red flag. We would like to see these improve before we get too confident of a rebound.

Economic data will be light next week. We’ll get some info on housing and durable goods, and that’s about it.

The big news will come from the central banks. The Fed is holding their annual symposium in Jackson Hole and policy changes are often discussed at the event. Leaders of our Fed and the European Central Bank will hold discussions and investors will be watching closely.

Investment Strategy

We weren’t surprised to see stocks rebound higher early in the week after last week’s selloff. However, we were surprised when stocks sold off so strongly later in the week.

One item we’re keeping an eye on is market breadth. “Breadth,” without getting too specific, is the amount of stocks moving higher versus ones moving lower.

The chart below shows that starting in late July, more and more stocks were moving lower and the amount of bullish (or positive) stocks and the amount of stocks trading below their recent averages has also been trending lower. Yet the market remained high. This is a red flag. We would like to see these improve before we get too confident of a rebound.

There are a number of stocks that are trading at attractive levels to us on a short-term basis. As mentioned above, though, we remain cautious as there’s still some weakness out there and we’re also approaching a volatile period for the market, so we are keeping a short-term perspective here.

As for our longer term view, our outlook is a little less rosy but still positive. We were hoping to see some pro-business reforms being implemented in Washington – lower taxes, regulations, etc. – but the likelihood of any significant reforms has diminished. The overall business climate is still favorable, which we think will still help the market.

Bond prices have risen and their yields falling, and we believe yields will stay low and prices high for the foreseeable future.

As for the rest of the portfolio, bonds to protect against inflation, or TIPs, remain a good long term hedge for inflation. Floating-rate bonds will do well if interest rates eventually do rise.

Some municipal bonds look attractive for the right client, too. We like buying individual, insured names for these bonds, avoiding muni index bonds if possible. We keep a longer term focus with these investments.

Gold is another good hedge for the portfolio. It is only a hedge at this point – rising on geopolitical issues as a flight to safety.

Finally, in international stocks, we see weakness around the globe and favor neither the developed or emerging markets, though they are looking cheap.

Please note, these day-to-day and week-to-week fluctuations have little impact on positions we intend to hold for several years or longer. Our short and medium term investments are the only positions affected by these daily and weekly fluctuations.

This commentary is for informational purposes and is not investment advice, an indicator of future performance, a solicitation, an offer to buy or sell, or a recommendation for any security. It should not be used as a primary basis for making investment decisions. Consider your own financial circumstances and goals carefully before investing. Past performance cannot guarantee results.

As for our longer term view, our outlook is a little less rosy but still positive. We were hoping to see some pro-business reforms being implemented in Washington – lower taxes, regulations, etc. – but the likelihood of any significant reforms has diminished. The overall business climate is still favorable, which we think will still help the market.

Bond prices have risen and their yields falling, and we believe yields will stay low and prices high for the foreseeable future.

As for the rest of the portfolio, bonds to protect against inflation, or TIPs, remain a good long term hedge for inflation. Floating-rate bonds will do well if interest rates eventually do rise.

Some municipal bonds look attractive for the right client, too. We like buying individual, insured names for these bonds, avoiding muni index bonds if possible. We keep a longer term focus with these investments.

Gold is another good hedge for the portfolio. It is only a hedge at this point – rising on geopolitical issues as a flight to safety.

Finally, in international stocks, we see weakness around the globe and favor neither the developed or emerging markets, though they are looking cheap.

Please note, these day-to-day and week-to-week fluctuations have little impact on positions we intend to hold for several years or longer. Our short and medium term investments are the only positions affected by these daily and weekly fluctuations.

This commentary is for informational purposes and is not investment advice, an indicator of future performance, a solicitation, an offer to buy or sell, or a recommendation for any security. It should not be used as a primary basis for making investment decisions. Consider your own financial circumstances and goals carefully before investing. Past performance cannot guarantee results.