An active week saw stocks end with mixed results. For the week, the Dow was higher by just 0.05%, the S&P rose 0.8%, and the Nasdaq was higher by 1.0%. Bonds saw a lot of movement but ended with little change. Gold was flat, too, down just 0.02%. Oil was also flat, down just 0.06% to $68.68 per barrel. The international Brent oil was lower by about $1 to close at $73.42.

The week was a busy one on a variety of fronts. There was another load of corporate earnings, a few important economic reports, several central banks holding policy meetings, and trade issues continued to grab headlines.

We’ll start with corporate earnings, which have been a very good story. About 80% of companies in the S&P 500 have reported their results for the second quarter and those earnings have been well above initial estimates. According to Factset, earnings have risen 24% over the past year, above the 20% initial estimate.

Companies have been rewarded with those beats, too. Bank of America Merrill Lynch reports that companies who beat their expectations saw their stock prices rise 1.5% on average. This is the best reward in two years.

We’ll start with corporate earnings, which have been a very good story. About 80% of companies in the S&P 500 have reported their results for the second quarter and those earnings have been well above initial estimates. According to Factset, earnings have risen 24% over the past year, above the 20% initial estimate.

Companies have been rewarded with those beats, too. Bank of America Merrill Lynch reports that companies who beat their expectations saw their stock prices rise 1.5% on average. This is the best reward in two years.

Apple’s earnings got a lot of attention as they turned in their best quarter for sales ever. This pushed their stock price higher and caused their market cap (or market capitalization or market value) to cross the $1 trillion threshold. That makes them the first company in history to be worth $1 trillion.

The market value of a company is found by multiplying the share price by the amount of shares outstanding. Apple has 4.83 billion shares, multiplied by over $207 per share bring you to that $1 trillion level. We’d urge caution here, though, since historically stocks tend to fall after the hype of reaching big milestones.

The market value of a company is found by multiplying the share price by the amount of shares outstanding. Apple has 4.83 billion shares, multiplied by over $207 per share bring you to that $1 trillion level. We’d urge caution here, though, since historically stocks tend to fall after the hype of reaching big milestones.

Switching gears to the central banks, where the Fed held a policy meeting this week. They announced no changes to their economic policy that has been stimulating the economy. However, they look poised to pull back on their stimulus by raising interest rates (which makes it more expensive to borrow money) at their next meeting in September.

One interesting point to note, in their economic commentary, they referred to the economy as “strong.” They haven’t called the economy strong since 2006.

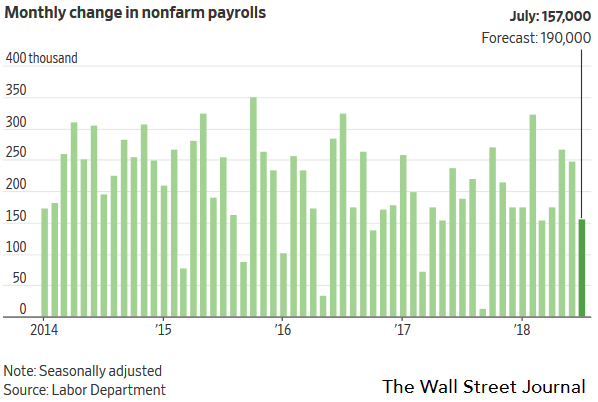

On the economy, the big economic report released this week came on Friday with the monthly jobs report. The economy added 157,000 jobs last month, which isn’t bad but was well less than the 190,000 expected.

However, much of the blame was attributed to the closing of Toys ‘R Us stores across the country which accounted for 31,000 job losses. Also, the last two months were revised higher to add almost 60,000 new workers, so the jobs picture still looks solid.

However, much of the blame was attributed to the closing of Toys ‘R Us stores across the country which accounted for 31,000 job losses. Also, the last two months were revised higher to add almost 60,000 new workers, so the jobs picture still looks solid.

Other economic data was mixed. Existing home sales fell for the sixth-straight month while prices rose. Incomes and spending both look solid. The strength of the manufacturing and service sectors continues to expand, though at a slower pace. Lastly, inflation continues to pick up.

Lastly, trade got a lot of attention as the Trump administration announced the possibility of raising the next round of tariffs from a 10% tax on Chinese imports to 25%. Our markets wobbled on the announcement, but eventually rebounded. China, on the other hand, has seen a large selloff in their market. This something that is not talked about here in the US.

The Trump administration cites the fact that the Chinese have devalued their currency significantly over the last two months as a reason for this decision. This is done to make their exports cheaper, which is important if you are facing a tariff that will raise prices 10 or 25%.

The falling currency may make your exports cheaper – but makes everything else in your country cost more. The Chinese people are seeing their costs rise while their stock market falls and economy slows – which is putting pressure on their government. This hasn’t gotten a lot of attention here, but it gives us the upper hand in these trade negotiations.

Next Week

Next week looks a little quieter. We’re getting closer to the end of earnings season and for economic data, we’ll get info on inflation and employment. Tariffs will probably be in focus again as the tit-for-tat with China continues.

Investment Strategy

Still no change here. This doesn’t look like an attractive time to put new money in the broader market, though there are some opportunities in individual stocks especially in the tech and small-cap space. We aren’t selling at this time, though, and don’t see the warning signs of a large pullback coming.

There is no change in our longer term forecast, which remains difficult to predict. Fundamentals are still very good with pro-business policies out of Washington providing a solid tailwind. However, rising interest rates have historically pulled markets lower. It’s tough to say where we think the market will go the long run.

Bonds are also volatile at this time. Yields have risen recently (and prices have fallen), but we don’t think prices will fall much further and continue to trade in the range they have been in for the last several months.

As for the rest of the portfolio, bonds to protect against inflation, or TIPs, remain a good long term hedge for inflation. Floating-rate bonds will do well if interest rates do rise.

Some municipal bonds look attractive for the right client, too. We like buying individual, insured names for these bonds, avoiding muni index bonds if possible. We keep a longer term focus with these investments.

Gold is another good hedge for the portfolio. It is only a hedge at this point – rising on geopolitical issues as a flight to safety.

Finally, in international stocks, we prefer developed markets to emerging ones at this time.

This commentary is for informational purposes and is not investment advice, an indicator of future performance, a solicitation, an offer to buy or sell, or a recommendation for any security. It should not be used as a primary basis for making investment decisions. Consider your own financial circumstances and goals carefully before investing. Past performance cannot guarantee results.

Next Week

Next week looks a little quieter. We’re getting closer to the end of earnings season and for economic data, we’ll get info on inflation and employment. Tariffs will probably be in focus again as the tit-for-tat with China continues.

Investment Strategy

Still no change here. This doesn’t look like an attractive time to put new money in the broader market, though there are some opportunities in individual stocks especially in the tech and small-cap space. We aren’t selling at this time, though, and don’t see the warning signs of a large pullback coming.

There is no change in our longer term forecast, which remains difficult to predict. Fundamentals are still very good with pro-business policies out of Washington providing a solid tailwind. However, rising interest rates have historically pulled markets lower. It’s tough to say where we think the market will go the long run.

Bonds are also volatile at this time. Yields have risen recently (and prices have fallen), but we don’t think prices will fall much further and continue to trade in the range they have been in for the last several months.

As for the rest of the portfolio, bonds to protect against inflation, or TIPs, remain a good long term hedge for inflation. Floating-rate bonds will do well if interest rates do rise.

Some municipal bonds look attractive for the right client, too. We like buying individual, insured names for these bonds, avoiding muni index bonds if possible. We keep a longer term focus with these investments.

Gold is another good hedge for the portfolio. It is only a hedge at this point – rising on geopolitical issues as a flight to safety.

Finally, in international stocks, we prefer developed markets to emerging ones at this time.

This commentary is for informational purposes and is not investment advice, an indicator of future performance, a solicitation, an offer to buy or sell, or a recommendation for any security. It should not be used as a primary basis for making investment decisions. Consider your own financial circumstances and goals carefully before investing. Past performance cannot guarantee results.